By Kumar David –

Prof. Kumar David

All countries except a few are in an inexorable and deepening debt trap; Dodging debt’s death-spiral is a vain hope

The well-known American economist Irving Fisher wrote “The Debt-Deflation Theory of Great Depressions” in 1933; its full relevance is unfolding now. Though Fisher is deemed the founder of the now discredited theory of neoliberalism, this paper is seminal; debt today is an ubiquitous ailment. In mighty USA government debt is $18 trillion or 105% of GDP and rising, Japan (250%), Italy (130%), France (95%), UK (90%) and to a degree Germany (65%). Little Greece (175%), Lanka (78%, $55 billion) and a legion other miserable minions are in a deep hole. The few not afflicted by spiralling debt are China (20%), oil-rich kingdoms and sheikdoms of the Middle East, Taiwan (36%) and South Korea (40%). The national debt of Singapore reads 115% but that’s an accounting oddity since large sums are stashed away by foreigners in the city state. These few examples apart all the world’s awash in debt.

An aside about Japan is that it is a “construction state” where politicians, criminal syndicates and bureaucrats coordinate to invest in exorbitant projects (some utterly inane like the “bridge to nowhere”). Projects are financed by debt funnelled from the public via taxes and mandatory savings at rock-bottom interest rates; everyone is required to deposit savings in accounts run by the post office. The huge debt overhang is all domestic, not foreign. Another useful bit of data to know is about foreign reserves. The top five are China ($3 trillion), Japan ($1.3 trillion), Switzerland ($700 billion), Saudi Arabia ($500 billion) and Russia ($450 billion).

Ok let’s get back to the debt-spiral. Fisher’s term of choice ‘debt-deflation’ was influenced by the circumstances of the Great Depression. Many have brought his concept up to date in the context of 21-st Century economic trends (for example J is for Junk Economics, Michael Hudson, publisher SLET, 2017). I propose ‘debt-spiral’ as a more appropriate term for today then debt-deflation. The bottom line is this; if a country (or a person) sinks too deep into debt it’s a pit of no return. It is not possible in the context of current global realities to beat a return to growth and liquidity even with austerity and “wise” policy choices. Greece from 2012 to today is a living example; the road from hyperinflation to Hitler is history’s horror story. The ECB, Germany and the IMF drove policies that goaded Greece into crisis; more on that in a moment after a bit of theory.

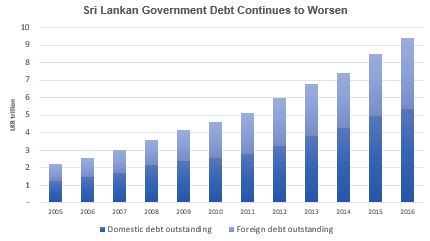

Sri Lanka debt outstanding (lower part domestic, upper part foreign)

Source: Central Bank

A trivial version first: Say a country’s (or individual’s) debt is 100% of GDP and the average interest rate 5% but the growth rate only 4%. Indebtedness will rise by 1% and there will be no surplus to invest. Consumption has to decline and the government, say Yahapalana will be ostracised. Indebted countries face the mathematical terror of compound interest unless exports rise quickly enough to pay down foreign debt really fast – a Sanderatne El Dorado? At 6% compound interest debt doubles in 12 years and rises four-fold in 24 years. (A rule of thumb is 72 divided by the compound rate is the years to double. At 10% compound growth a quantity will double roughly in 7.2 years and double again every further 7.2 years. Use it, the 72-Rule is a useful guideline).

A complication is that when debt grows a stage is reached when one needs to borrow to meet interest on current liabilities thus pushing one ever deeper into the trap. This truism economic pundits pussy-foot around at seminars and in newspaper columns. There is no salvation but to write off debt, however creditors and global finance capital – the 1% – won’t stand for it. Lanka maybe faces an average interest rate of about 5% and US 10-year bond yield is about 2.5%. Furthermore, say a fiscal deficit (budget deficit) of 3% is also unavoidable (or do you want revolution?). This will add another percentage point or so to annual borrowing needs. This is a double whammy and descent into the spiral accelerates. US government debt is forecast by web-site ‘Statistica’ to rise to $34 trillion by 2028. The Congressional Budget Office says it will be 150% of GDP by 2048 and interest payment will be 6.3% of GDP. Trump’s recent corporate tax cuts would have eroded these numbers further.

This is not the end; there’s a third whammy. From 2008 central banks and Western governments have bailed out banks and bondholders with direct handouts and injecting huge sums – quantitative easing (QE) which has now reached a cumulative $3 trillion. QE is not to be confused with Keynesian state led spurring of the real economy to raise production and employment. The beneficiaries of QE are banks, bondholders, property owners, stock-market investors and Ponzi operators. The 99%, the public, do not benefit from QE which is offered to finance capital and global Wall Streets at large. A similar story is true when interest rates are held down to the floor encouraging financial bubbles. QE has led to a boom in asset prices (equities and real estate) benefitting the 1% and impoverishing the 90% – the 9% in between has had mixed luck. Absurdly the US 10-year bond yield hovers below the rate of inflation providing the government with a temporary free-lunch bonanza till the Fed is compelled to raise rates. There is so much froth building in US assets that a stock-market bust seems very likely.

Interest payments and debt trimming diverts money from capital expenditure and from production and employment creation. The Troika, IMF, ECB and European Commission, bailed out no not Greece – perish that thought – but super-rich creditors and bank bond holders and equity owners. Greece was NOT bailed out, German and European finance capital WAS. Greece continues indebted to new overlords the Troika, instead of German and European financiers. Yes, “Haircuts” (reduction of interest on some debt was allowed) and complex repayment schedules were introduced. In exchange unbearable austerity was enforced. As James Galbraith noted “There is no rescue going on. What is going on is SEIZURE of assets owned by the Greek state, businesses and households. This has nothing to do with the recovery of the Greek economy”.

Seizure? When an economy crashes, privatisation is enforced and finance capital grabs public assets for a song as in Russia in 1990-95. When a country is unable to deal with debt for reasons outlined before, the final denouement is to downgrade credit-rating and declare it credit unworthy. In quick order the economy collapses (Argentina, Russia in 1990-92, Greece, Mexico and Pakistan) and privatisation is enforced as Galbraith says. China’s grab of Hambantota Port in a 99-year lease is similar.

A bitter truth is that IMF insistence on austerity during economic downturns is counterproductive. Government spending in a downturn is vital stimulation; a prescription as old as the New Deal and Keynesianism – of course that spending must be wise. Austerity (conditionality) enforced by the IMF on near insolvent countries takes money out of the productive economy, QE injects liquidity into private money markets and rock bottom interest rates lubricate acquisition of public assets by domestic and foreign capital. The IMF, IBRD and ADB are conscious of their class motives; they are knowingly with the 1%. Nowadays they do not have to pretend to be much interested in the 99%.

Indrajit Coomaraswamy, bless him, his stalwart efforts notwithstanding, cannot stand against the tide of history. He is the uncle of my buddy Jayantha, a peripatetic preacher in Australia, who beholding all the world arraigned against his uncle is leading prayers and lighting candles for the salvation of his immortal soul. Bless them both but it’s a tough call when global finance capital stands against you. The bar-chart reproduced from Central Bank sources shows inexorable growth of indebtedness – I don’t have 2017 but the trend is unlikely not have reversed. The trend cannot be written off merely as Paksa clan thievery. In a recent column I estimated the family’s global treasure at about $0.1 billion. Lanka’s indebtedness of $55+ billion is much larger and the trend more systemic than can be attributed to graft. Corrupt governance, illicit deals with the Chinese and the like matter, but the underlying trend is global. Water flows downhill thanks to gravity; in Sri Lanka it went down with the sewage.

In ancient times, kings and emperors wiped all debt clean every so often, maybe every five to ten years or on some auspicious occasion like victory in battle or the birth of an heir. At the end of WW II all German debt was forgiven making possible the miracle German recovery. Wiping off debts of farmers and tradesmen in the ancient civilisations of Mesopotamia and Egypt let agriculture, handicraft and trade make a fresh start. The relevance to modern times is that now like then, debt is mounting inexorably from production cycle to cycle and cannot be cleared by intrinsic mechanisms. There has to be some debt write off. A laxative will relieve Indrajit’s constipation and ease Jayantha’s supplications.

Debt forgiveness is bitterly opposed by the 1% – bond holders – not only in the Greek case but everywhere; think Argentina and Africa. If all the world’s in debt, who the creditor pray? There has to be someone on the other side of the balance sheet. Ha you’ve hit the nail on the head! It’s the 1% (or 10% depending on how you count the cash) which holds 80% (what did Piketty estimate?) of global wealth. Global state-debt may be $75 trillion, say four times US government debt (I am using the logic that US GDP is a shade below a quarter of world GDP). About a third of US government borrowing is from the Social Security Trust Fund and pension funds, nominally owned by the people. Likewise I conjecture the creditor of two-thirds of all global debt is global finance capital that is the 1%. My guess could be off by five or ten percent, but surely not more. The moral of my story is that the peoples of this planet are in eternal hoc to the super-rich, the super-swamp.

justice / September 9, 2018

This is all very well, but the author should review the Sri Lanka situation and suggest remedies for same.

/

Don Stanley / September 9, 2018

Kumar you talk as if Debt is the fate of the world!

This is patently NOT the case. Debt is the result of financialization, political corruption and neoliberal economic policies of the IMF, WB and ADB– in Sri Lanka.

The Washington-Tokyo agenda to put Lanka in the permanent bailout business and then asset strip the country while militarizing Lanka and weaponizing religious conflict (Buddhist-Muslim) to distract us in their New Cold war with Bondscam Ranil as their partner.

Critical thinking and human development focused policies with a zero tolerence of corruption is the solution to the corruption racket that IMF-WB_ADB promote to benefit global 1 percent.

You are right that “From 2008 central banks and Western governments have bailed out banks and bondholders with direct handouts and injecting huge sums – quantitative easing (QE) which has now reached a cumulative $3 trillion. QE is not to be confused with Keynesian state led spurring of the real economy to raise production and employment. The beneficiaries of QE are banks, bondholders, property owners, stock-market investors and Ponzi operators. The 99%, the public, do not benefit from QE which is offered to finance capital and global Wall Streets at large.”

Lanka must stop following the US model of rewarding the corrupt and needs to prosecute financial criminals (Rajapaksa and Ranil and cronies), take over their assets and end the political culture of impunity and immunity for FINANCIAL CRIMES.

/

Native Vedda / September 9, 2018

Don Stanley

–

Could you define and explain what you mean by “financialization, political corruption and neoliberal economic policies”.

/

edwin rodrigo / September 10, 2018

I agree. It is well known that IMF, WB are at the root of the trouble. They are responsible for the destruction in many poor countries and the death of so many people in them. It is strange that Prof David being a Professor of economics, does not even mention the role of destruction played by these institutions.

/

K A Sumanasekera / September 9, 2018

Dr Kumar’s Figures on National Debt of the Western Countries are pretty much in the Ball Park.

But his figure of our Lankawe is, way off the mark.

For Example Dr Ranil and his Robber Brigade has pushed our national debt over 80 % .

In fact it is 82 percent says my Elders.

–

For that extra 6 to 7 Percentage increase, Dr Ranil and Dr Coomarasamy have nothing to show in Infrastructure or Economic Development.

All they have are Melia and Onelia’s Luxury Pad and Aloysiou Families 24 Businesses in Kolombothota…

-.

With regards to the so called Rajapaksas loot , Dr Kumar is totally out of whack.

Current UNP stalwart and the main Bouncer of Dr Ranil’s Yahapalana Cabinet and the world’s best Health Minister gave eye witness news, that he found USD 18 Billion in a Arab Bank which Rajapaksas have deposited,

The HM’s mighty Son and a potential future Leader of the UNP , young Rajitha swore to the Media that the Arab bank Boss took the Young Rajitha on a special tour of the Bank Vault.

And he swore that he saw all the Bags lying on the Floor all stacked with Green Backs.

The current Finance Minster Mr Samare informed the Media that his Western Intelligence Contacts confirmed that Rajapaksas have stolen USD 18 Billion.

Where the hell Dr Kumar got that USD 0.1 Billion figure ?

/

Native Vedda / September 9, 2018

KASmaalam K A Sumanasekera

–

“For Example Dr Ranil and his Robber Brigade has pushed our national debt over 80 % .

In fact it is 82 percent says my Elders.”

–

Could you tell us 80% and 82% of what.

By the way your Elders have been always wrong.

–

Not just Arab banks but the banks everywhere have been happy to launder stolen, drug, …..untaxed income, ………………….. They are willing to wipe your bum as well if you keep a minimum deposits in tens of thousands …. The managers will visit you when you need them with wipes.

Where do you keep your crumbs you got from the clan.

/

Mallaiyuran / September 9, 2018

Lankawe case is 80% of the GDP going to loan service. Practically only 20% left for budgetary spending. That is why Yahapalanaya is borrowing to pay the 10,000Rs increase it gave to government servants.

“A trivial version first: Say a country’s (or individual’s) debt is 100% of GDP and the average interest rate 5% but the growth rate only 4%. Indebtedness will rise by 1% and there will be no surplus to invest.”

Why the professor made this calculation so completed.

Let’s put some assumption, so we can make it simple. Say it is strictly a country- no individual. There is no compound interest. Everything is Simple Interest. As of today the budget is balanced, of cause with the loan in the background. Now let’s make some of the percentages as $ value. The loan is not 100% of GDP but its $100 and equal to loan. Government Service expenditure is $80. Loan service is $5 interest + $5 principal+$5 escrow.

Now we can redo the calculation. What is now left for growth is =(GDP $100- Social Service $80- Loan Service $15)=$5. Next year the story will be different. Loan service will go down if the payment is not an annuity. We approximate through Escrow and interest to $14. GDP faced 4% growth so next year GDP is $104. We need to revise our calculation for next year. I.e: $(104-80-14)=$10. This year the capital growth (investment) was only $5 but next year it is doubled to $10.

His leftist mind is interpreting Hangbangtota selling as privatization. He could not find a word for Colombo Pong Cing sale. So he just ignored it. These are foreclosures of white Elephants. Nationalization is a policy matter even on accounting profit earning government operations. Because accounting profit calculation needs not to match theatrical Economic profit. Privatization is always reducing economic loss and increase profit.

/

Mallaiyuran / September 9, 2018

Rest of his calculations has unnecessary complication & thus guiding to confusion. He is trying to compare US 2.5% bond rate with Lankawe Interest rates. You can’t compare US bond rate to US interest. Bond might have been discounted, that is not possible in loan. You can’t compare US interest rate to Lankawe interest rate because yearly Exchange rate variation and inflation variation between countries. US bond rate is 2.5%. But in 2015 March Central Bank was forced to sell at 12%. Further bond rate is fixed by governments. But one has to look at how much is subscribed at that rate too. If Lankawe had fixed at 5% in 2015, then it may not have got even 10 Million rupees. But at 12% it got 11 Billion.

Then he is confusing with internal borrowing as good instead of external. So he thinks Japan is doing better with its 275% of GDP. But if you look at India, it is growing above 7%. America just recently reached to 2.5% . But within the last five years, Indian rupee has fallen from 35 rupees to 70 rupees. Though India is growing faster, it is not showing on the exchange rate. America is not able to take advantage of Indian growth but because of exchange, losing ground. So the better deal for America is find some way the exchange rate tightening will relax so American manufactures too can sell something to India. More America borrow from outside, more Dollar lose ground and better for export. Japan is not in currency exchange business, they don’t face the dollar’s artificial increase against other currencies just by the exchange business. His entire essay needs to be rewritten by economists, not by an engineering Professor like Kumar David.

/

HRS / September 9, 2018

The Financial Times’ Gillian Tett was the star journalist from the mortgage finance Bubble period. I read with keen interest her piece this week, “Five Surprising Outcomes of the Financial Crisis – We Learnt the Dangers Posed by ‘Too Big to Fail’ Banks but Now They Are Even bigger.”

Tett’s article is worthy of extended excerpts: “What are these surprises? Start with the issue of debt. Ten years ago, investors and financial institutions re-learnt the hard way that excess leverage can be dangerous. So it seemed natural to think that debt would decline, as chastened lenders and borrowers ran scared. Not so. The American mortgage market did experience deleveraging. So did the bank and hedge fund sectors. But overall global debt has surged: last year it was 217% of gross domestic product, nearly 40 percentage points higher – not lower – than 2007.”

A second surprise is the size of banks. The knock-on effects of the Lehman bankruptcy made clear the dangers posed by ‘too big to fail’ financial institutions with extreme concentrations of market power and risks. Unsurprisingly, there were calls to break them up. The big beasts are even bigger: at the last count America’s top five banks controlled 47% of banking assets, compared with 44% in 2007, and the top 1% of mutual funds have 45% of assets.”

A third counter-intuitive development is the relative power of American finance. In 2008, the crisis seemed to be a ‘made in America’ saga: US subprime mortgages and Wall Street financial engineering were at the root of the meltdown. So it seemed natural to presume that American finance might be subsequently humbled. Not so. American investment banks today eclipse their European rivals in almost every sense… and the financial centres of New York and Chicago continue to swell…”

/

Rajan Hoole / September 9, 2018

I have for many years seen Kumar David dealing with the larger picture, which is certainly frightening, one which the world leaders have no doubt got to deal with. In the last Century we had two World Wars which made life and living very unpredictable and, apart from myriad lives, lots of properties and savings were wiped off. People in the North-East of this country too experienced the fickleness of planned existence.

But I think countless ordinary individuals who have their day to day lives to deal with, will shrug off the larger picture and continue planning and saving for the future of themselves and their families in the usual way. Several banks and companies that enable modest savers to invest in shares and equities all over the world, despite the vagaries of business cycles and regular financial crises, have served investors fairly well over many years. This is not to diminish the importance of the larger picture, but for families and individuals, life must go on.

/

Hema Senanayake / September 9, 2018

This big picture is important. Kumar David has observed that, “but the underlying trend is global.” It is true because the problem is systemic. A recent study has pointed out that the system’s credit growth must be faster than the GDP growth. Systemic credit includes debt of public debt, consumer debt, margin debt (in stock market) and non-financial business debt. If debt must grow faster than GDP there is no wonder that almost all mature economies must post “over indebtedness.” The world must awaken to this reality first. Sri Lanka too, has this problem and also a lot of economic mismanagement. If Sri Lanka can take control of the country’s current account and Balance of Payment with non-credit based sources, at least we can have a little hope as entrepreneurs could take care of the rest for the time being. so that lives of families and individuals could go on. Thanks for your great comment.

/

JD / September 9, 2018

KUMAR DAVID’s figures are lies. Japan 250% is mostly to it’s own citizens who went against the govt and saved money. On the other hand, USA has 50 million in poverty, probably another 50 million unemployed. there the Srudent loans defaults, Housing market economy collpahses. Multipla eExecutive Owning Lehman brothers crashed the economy because of their fuinancial experiments. anyway U”SA “debt is diluted as the Dollar is international and Quantitative easong (think and see) dilutes the debt. Their debt is mostly owned by other countries as the dollar is superficially jacked up. Think about if Sri lankan rupee is devalued to meet a GDP/DEBT ratio of 105. BY the Way, Sri lanka’s GDP is mostly SERVICE ECONOM”Y driven. Even the women in the middle east and men in South Korea as Service sector. Sri lanka’s manufacturing economy is less thabt $ 2 billion. Even if it brings back (because businessmen deposit in foreign banks) not enough to sustain the country. Itis the west give loans asking people to borrow. go and spend in a vacation.

/

JD / September 9, 2018

I am wondering whether the objective of your article is to provide VISION to RANIL (HARVARDS” team definitely that is excellent idea) of the he Sri lankan govt to declare bankruptcy and get rid of debt. I think that is good too. Because,. Mangala and RAvi the LIAR established legislation and required infrastructire for foreign hands to take over what evr valuable in Sri lanka. Now, when the govt say we are bankrupt and no money to pay, they say we can not go empty handed and givee some of your assets to us. Dollar is Rs 162 ?, so they will buy everything almost free. Sri lankans will sweat for nothing and they will just live because they can not committ suicide when the govt has already made the country commit suicide.Check what happened to the most developed country in North Africa Libya, what happened to it. Gadhaffi talked about GOLD backed Dinar He is gone. CHAVEZ in Venezyela talked a similar language befire he was taking the Polonium cocktail and die. NOw their money is also like ZIMBABWE some time ago and China came and saved them.

/

K.Pillai / September 9, 2018

There was the hunter-gatherer. Then came tribes. Bartering followed and perhaps the pawning thingy. Then ‘money’ was invented. This led to lending and borrowing which led to the ingenious concept ‘interest’. Shylocks appeared, the banks and ‘debt’.

Most surprising outcome is the use of ‘debt’ as a commodity. It is bought and sold often profitably.

.

This ‘debt’ thingy is bound to lead to wars. It is as destructive as climate change.

Kumar David and others look at the ‘debt’ industry via various ‘ratios’. Is it time to address how it is created and sustained?

/

Native Vedda / September 9, 2018

K.Pillai

–

You missed how surplus was stored.

/

Mallaiyuran / September 10, 2018

“ The beneficiaries of QE are banks, bondholders, property owners, stock-market investors and Ponzi operators.” , (what the heck is that, coming here. Subject here is economic analysis not criminology)

He (prof. Kumar) is not providing any vision for anyone. He is the naughty boy who ran to Scotland and on his way he came across a mighty elephant and he wondered standing in his shoes “Oh what a big loan”. That is how his vision of big picture. His favorite hobby of storytelling can be spent with grand kids, telling how the Astra in Mahabharata and Ramayana flew faster the than American & Russia Missiles!

He is so confused so he is mixing the wealth distribution with the QE – monetary market operation. Then he came out with his new Marxian inventions that the QE is a mechanism to transfer the wealth from 99% to 1%. Let me ask a question: Is Old King is bigger hero in LG election by asking “You want one Country or Two Countries” or Prof. Kumar is greater hero by making a story to CT Modayas, the cream of the IQ 79s, that QE is transferring wealth from poor to rich? Come on Guys, this is not astrophysics. I think Hawking did not die, he committed suicide!

/

Mallaiyuran / September 10, 2018

QE started by Obama (Bernanke), a people’s president, not by Trump or Bush. When the AIG failed Uncle Sam invented a way to bail out the banks. AIG was guaranteed as “Cannot fail” but it did. When the lake is dried, fishes expect water to flow through the river. In this case River dried. Unless somebody find a way to make water to flow back in to lakes, it was a, to be history, worse than 1930s. So government said to banks it will take the assets (restricted) and pay them money for those assets. These assets were understood as bankrupt payers. Banks cannot claim insurance; after all they had paid their premiums for this purpose. The assets were not productive and would not yield any money. Because of the legal & accounting matters the assets held on the book and evaluated. When Uncle Sam paid the money for those assets, bank were back again on the rolling business. There is lot of other matters. We have to only stand near to the shore and judge the depth of the water in the middle of the sea. This is of complicated housing loan lending. The Banks mainly in that were not the commercial banks (Fannie Mae and Freddie Mac.). Once the banks start to see the water, clients can reengage in buying homes. Here no 99% or 1% story. The housing loan crash affected the entire society. When AIG collapsed the pain felt through many dimension. The marrow minded prof, still under 100, but his ideas are older than Marx, over 200 year backward, just inventing a lot on areas he has no clue at all. So how Uncle did fund this extravaganza? The government loan went from $5.8 Trillion to $14 Trillion. But the actual recovery took place made much more trillions to flow through the people’s hand. Because some bonds also bought back, now government is holding its own bonds. Hard to grasp that, as well as funny, but still that gambling turned around the economy.

/

Mallaiyuran / September 10, 2018

One should note the difference of selling the Colombo Pong Cing and Hangbangtota Port and land, then government creating the White Elephants and US government buying back its bonds and underperforming assets from public banks so they can redo the private lending. These are North Pole – South Pole actions. Our engineering professor is comparing them equally to get hurray from IQ 79s. Comparing North Pole & South Pole is not big picture, but bigger, bigger picture.

GDP growth rate is not the one decide to borrow “more” or no. If the ROI is higher than interest rate (or marginal rate of return), one can keep borrowing (Provided quantitative result is the only constraint we have), if interest has gone above ROI then bonds are the good ones to buy with the money in hand. So when, where, who, how much one can borrow is the biggest picture, for that analysis, our Prof. had not been trained to take a dissection set between his fingers.

“Government loan/ GDP” tells nothing for an average person. Bringing that misleading number here is like Old Royals crowd gathering in Colombo with Arrack. Absolute, outrageous crime!

/

babloo / September 10, 2018

Why doesn’t the author give the % and the amount for India? Perhaps, that is because this article is based on some thing that is originating in the West. We know that the author does not have any new ideas and the same recipe and ingredients are used over and over again.

/

Maurice / September 10, 2018

The Pundits who attempt to discuss the big picture always get it wrong. The polticians who begin to believe in such “big pictures” carry out the dicta of the big picture and create gulags.

Not so long ago Kumar David subscribed to the “BIG PICTURE” where it was claimed that historical materialism will “INEXORABLY” drive the world to the class conflict culminating in a worker’s revolution followed by Paradise.

Kumar David spent much of his life preaching it and profiting from it, and many lower level people (workers in the GCSU etc) controlled by the LSSP trade unions got killed in various “Hartals” organized to topple the government and usher in “the revolution”. The youth were trained to disrespect the law and attack the police. The JVP did what the LSSP preached, while the LSSP merely talked., and so th JVP killed thousands of innocents. Then the goons killed thousands of other innocents.

When all that failed, Kumar David and the likes of Wickremabahu moved to support the LTTE “struggle” and moved directly into the Right Wing, supporting fascists like Fonseka when he ran for president!

Today Kumar David writes monetary analysis, supports the coal-power lobby, just like any western capitalist analyst. There is no longer a hint of the class struggle or historical materialism in this write up.

He now has another “big picture” diametrically opposed to his Marxist theories, that any US economics student’s term paper could have done justice, to get a B-plus.

/