By Kumar David –

Prof. Kumar David

Markets surge while fundamentals remain weak: Is capitalism on the global mend?

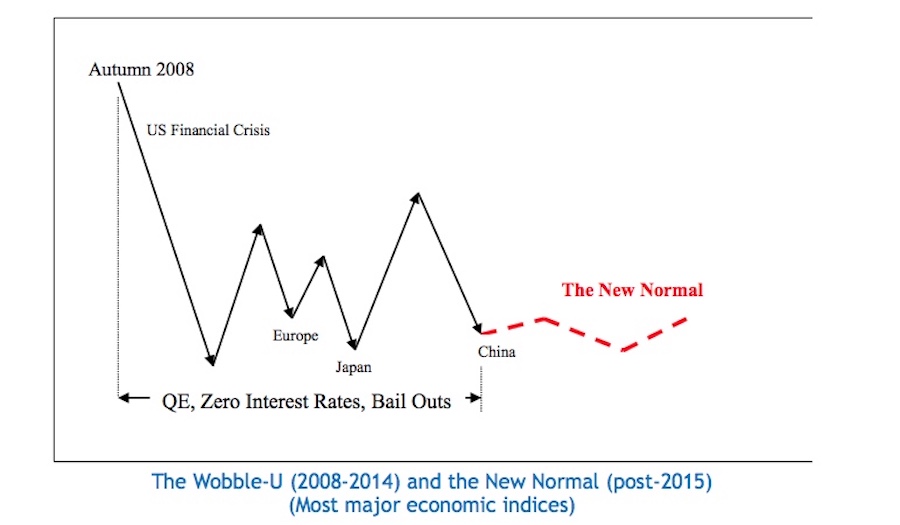

From the time of the crash of 2008, I have been among the voices that warned of a prolonged recession (I called it New Depression) which global capitalism would not climb out of for a protracted period. Though not as serious as the Great Depression of the 1930s, thanks to new recession fighting tools applied globally and the stabilising influence of China, global capitalism failed to achieve robust recovery for nine years, almost as long as the Great Depression. The last few months, however, have seen a rally of equity markets and a mildly encouraging upturn in growth rates, commodity prices and employment. So, has global capitalism finally got past the New Normal in my little diagram?

The diagram is the fruit of my theoretical musings in 2008 updated in 2015. It says that unlike after conventional recessions, there would be no ‘normal’ recovery; instead the global economy would keep bouncing about the bottom. ‘Wobble-U Shape’ I thought was a neat term to coin side by side with the familiar V-shape, U-shape and W-shape, for fast and slow recoveries and a double-dip recession. The 2008 slump in US financial markets and banks was followed by a downturn in Europe (aggravated by the collapse in Greece) and recession in Japan and then China slowed in 2014-16. For three years from 2014 both ‘one-handed’ and ‘two-handed’ economists accepted the New Normal, life at the bottom of the trough, as normal. This little figure has stood the test of time better than the offerings of conventional liberal economists and Nobel Laureates.

Now the interesting question is: “Has global capitalism entered a period of recovery in its boom-slump-crisis-(war)-recovery lifecycle?” – Marx’s organic cycles, inbuilt in capitalism’s nature. Or is this a false dawn again? The paradox is that though signals of recovery are strong, fundamentals are weak. I will have to return to the subject again and again in the coming months but for now I will confine myself to alerting readers to some developments. Though no economist, I have observed that people with a sound grounding in materialist science, wide reading and disciplined study, do better than professional practitioners of the ‘dismal science’ in making sense of the real world.

The most visible sign of recovery is the state of play in global equity-markets. The best-known indices are going through the roof; Dow* (32%), Nasdaq* (36%), NYSE (23%), S&P* (25%), Hang Seng* (41%), FTSE* (8%), France’s CAC (14%), Nikkei (22%), India’s Sensex (30%) and Shanghai (12%). The number in parenthesis is the rise in the last one year and an asterisk (*) means that the index reached an all-time high in recent weeks. Equities have soared this year in the US in part in response to Trump’s pro-business push for deregulation; American capitalists are optimistic that impending tax-cuts and public welfare reductions will buoy the well-to-do classes. But the market is volatile and driven by speculation; it an unreliable indicator of economic health. Markets are at heights not seen except in 2000 and 1929 – dotcom bubble and Wall Street Crash. The share-market is like sex, the best part is just before the end.

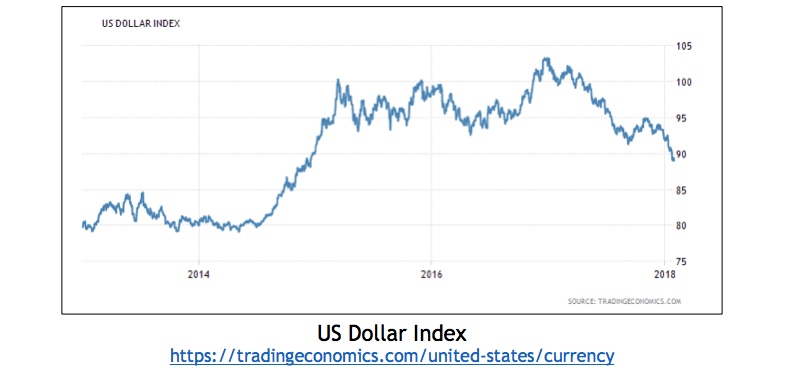

The dollar remained depressed after the 2008 recession for over six years till early 2014. It recovered smartly in mid-2014, declined again in early 2017 and remains on the low side. The index in the accompanying chart weights the dollar against a basket of currencies and started at 100 in 1973 when Bretton Woods was dismantled. Its all-time peak was 165 in February 1985, lowest 70.7 in March 2008 and it is 89 now.

Another feature is that bond yields are rising; the US benchmark 10-year has shot up to 2.7% and the 3-month Bill is at 1.4%. Rising bond yields (lower bond prices) signal declining confidence in government and economy. Loose money is fuelling an equity surge; Central Banks are priming the global financial system through Quantitative Easing. In an environment where capital is reluctant to undertake major productive investments at home or abroad, this encourages market volatility.

Weak fundamentals

U.S. trade deficits have been at the heart of a runaway expansion of a market driven financial bubble round the world. There is no will and no political climate to cut consumption and reverse trade deficits. American capitalism has caught a tiger by the tail. Dough Noland writes “The U.S. financial situation is unsound and untenable. The de-industrialised services and finance-based economy is hooked on on unending credit expansion, The U.S. boom is financed by unsound leveraging generated by global central banks and speculative finance. The perpetual outflow of U.S. ensures a crisis of confidence in the dollar”

The IMF has warned that the global economy’s recent recovery may not last, despite a pickup in activity in western countries. Marking the 10th anniversary of the onset of the financial crisis it said, in its World Economic Outlook Report, that governments will be lulled into a false sense of security by booming markets and ignore essential domestic tightening. Capitalist governments won’t touch the rich. The global economy will fizzle into a decade of sluggish growth in the 2020s as the current upswing fades and a slowdown in population kicks in.

World Bank analysts have said that they expect the world economy to grow by 3.1pc this year, following an improved 2016 as the shadow of the financial crisis is shaken off. But this will be the high point of a temporary recovery as underlying structural problems surface in the next decade. Weak productivity growth globally, poor levels of investment and an ageing global workforce will dent growth. “This is a cyclical recovery, it is a rebound from weak growth in 2016. Underneath that there is a slowdown in potential growth,” said Franziska Ohnsorge, economist at the World Bank.

“If you look backwards 10 years, potential growth has slowed by about 1 percentage point globally. Looking forwards we expect it to slow further. Potential growth for the next decade is estimated at about 2.3pc.” This World Bank forecast is based on a relatively benign scenario in which none of the big risks to growth emerge.

The political dimension

“The most likely cause for the bubble to burst would be the rising political tension in the West. The bubble economy keeps squeezing the middle class, with more debt and less wages. The festering political tension could boil over. Radical politicians aiming for class struggle may rise to the top. The US midterm elections in 2018 and presidential election in 2020 are the events that could upend the applecart”. Andy Xie in Hong Kong’s South China Morning Post 8 Oct 2017. I disagree, distressed fundamentals, not the political antics of neo-populists, are at the root of crisis.

In the previously quoted report the IMF says the backlash against globalisation, stoked by stagnant wages and the loss of well-paid, middle-skill jobs, is a threat to the global economy and noted that sustaining expansion requires abandoning protectionism and doing more to ensure that gains from growth are shared more widely. A decade after the financial crisis sparked economic decline around the world, 2017 seemed the year when capitalism came back. Failure by right-wing populists to seize power in Europe prompted stabilisation helping the single currency bloc to recover after years of tumult, while China kept up its rate of expansion despite fears over a sharp slowdown. According to the OECD, global real trade growth accelerated from 2.6% in 2016 to 4.8% in 2017 and world GDP growth moved up from 3.1% in 2016 to 3.6% in 2017.

Multinational agencies (IMF, World Bank etc) and establishment economists in global banks and corporations seem more concerned about political instability than unsteady fundamentals. I have a different view. Despite Trump the US will not plunge into political collapse; but trade imbalance, debt rising another $ 1.5 trillion in the next decade, and inability to service commitments in social security is far more serious. Though Theresa May will make a hash of Brexit, the already overdue Labour Government will be able to muddle things along. Neo-populism has not recently made gains recently in Europe; China is stable, Modi is ambitiously populist and likely to win the next Indian election.

In a word it’s not political instability but the fundamental systemic problems of the economy that are problematic. Unsustainable low interest rates and irresponsible monetary policy (QE) cannot go on, but Central Banks are terrified of the consequences of tightening. Strict spending controls seem undoable in Western Democracies and rising debt is out of control. The dollar is to be under pressure and worst of all capital is not interested in new investment. It’s the structure of the capitalist economy, not crazy neo-populists who threaten the house of cards down.

The implications of a short-term global rally are on the whole positive for Sri Lanka. Exports will rise and the rupee will stabilise if there is liquidity in Western markets and the dollar falls. On the other hand, rising global interest rates will aggravate our foreign debt servicing burdens. As for an ensuing long slump in the West, the way forward for Lanka is to expand its Asian businesses (China, India, Singapore and many others) as this is where our future lies.

Dr. Dayan Jayatilleka / February 11, 2018

Hey comrade Prof, how’s the “Porottuwa” or “Poroppaya” doing, eh? Ain’t you tired of getting it — and Mahinda–so wrong? First the war, now the election?

/

Thanos / February 11, 2018

Wow Dr. DJ. Just, wow. Can’t believe you, a person with a PhD, a person with a high level of intellect actually post stuff like this. This is more like what a your typical internet troll would post.

/

N Wimaladasa / February 11, 2018

The analysis and describe of Global Economy of ongoing recession and crisis has thousands of articles and books has been published by Western world writers and their think-tanks. Hence that Kumar David is nothing that new one is on here. But is not a Marxist ,but born Trotskyist oriented politics was belongs to outdated anarchism and adventures line of anti -Marxism by LSSP origin.

To be read his writing on that good for leisure time, that not give any practical solution of ills of Political-Economic-Social ongoing crisis our country and Globally that is an unattended by his school of thought . In fact Trotskyist having habits of long-writing -letters, which having shows that they are pundits are above other scholars in the our solar system and its plant.

On the other hand without diagnosed real issues of current world and local objectives conditions of by that level of economy and system of disorder of Monopoly capitalism that the so-called interpretations belongs to metaphysis world outlook.

That wont give any solutions for ills of current UNP regime that misrule and mismanagement in an Island entire Economy by all UNP S of Ranil Wicks, MS and CBK last 37 months.

The Kumar David….dodge most paramount issues of by CB has exposed — to —market risk ,interest rate risk, credit risk, liquidity risk ,and operational risk. By new complex organizational of emerging economics structure has been an emerge in New Globalization since 1990!

By an outdated that UNP type of misgoverning of CB and Economic policies are that including international FINACIAL CONGALOMERATES THAT POSE NEW challenges for existing regulation and guidance of policy supervision.

Under the new model of sustainability of Capitalism the services of both growth diversification and adjustment willing to sacrifice the very PROFIT. By any policy makers have to balance both trade and investment by the measurement and management of risk of the utmost important.

This simple fact of an Economy of growth and development New Global Capitalism that did not realized by David Kumar!

/