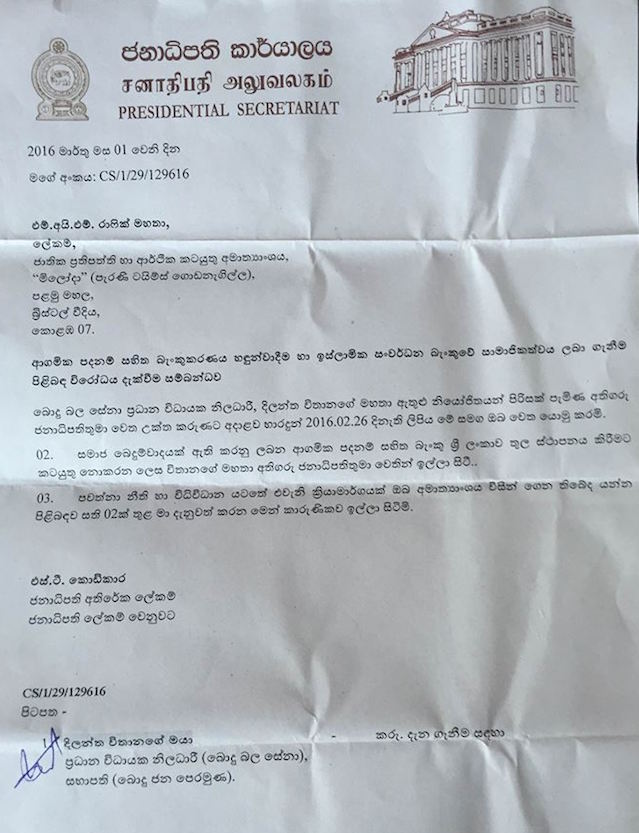

President Maithripala Sirisena has called for explanation from the Secretary of the Ministry of National Policy and Economic Affairs M. I. M. Rafeek as to whether the Sharia banking practice is been introduced to the country by following the respective laws and regulations of Sri Lanka.

Sirisena’s Additional Secretary, S. T. Kodikara, in a letter addressed to Rafeek has called for explanation within two weeks on the matter. Incidentally, the National Policy and Economic Affairs portfolio is held by Prime Minister Ranil Wickremesinghe.

Sirisena’s Additional Secretary, S. T. Kodikara, in a letter addressed to Rafeek has called for explanation within two weeks on the matter. Incidentally, the National Policy and Economic Affairs portfolio is held by Prime Minister Ranil Wickremesinghe.

The letter to Rafeek comes, amidst reports that the government is looking at introducing a new regulation to facilitate Sharia banking practices in the country, so it could obtain finance from Saudi Arabia to get out of the current debt ridden situation.

The letter to Rafeek was sent after the Bodu Bala Sena (BBS) Chief Executive Officer Dilanthe Withanage wrote to Sirisena claiming that the Central Bank Governor Arjuna Mahendran had gone against an earlier assurance and was going to introduce the Sharia banking practice in the country, which, according to Withanage would bring in social and religious disparity among communities living in Sri Lanka.

Withanage in his letter said, “Due to the failure of the leaders, and specially for a country where the majority is not Muslims, to enforce the Islamic Sharia Law in secret is cause for concern. Further, the Parliament’s silence on this matter is also a dangerous precedent. Therefore, I call on you take look into this matter.”

In a separate letter to Mahendran, Withanage said that this move was completely unacceptable with catastrophic consequences which will cause an irreparable damage to social cohesion and integration of different communities into mainstream society.

Withanage added that Sri Lanka must not sell its national identity to Saudi Arabia for US$ 1 Billion. ( By Munza Mushtaq © Colombo Telegraph )

Point of View / March 7, 2016

I thought we already have sharia banking in SL.

So sharia banking is not good for the country but the money earned from cleaning Arab toilets is welcome !

What hypocrisy ? MS too is playing to the gallery.

/

words / March 7, 2016

Sharia banking has been around for about a decade.. our idiotic president is showing that he is just that!:))))

/

Gamarala / March 8, 2016

It is unfair to blame the President.

The President’s letter has requested information from Ministry Secretary on whether they have followed the existing laws on this matter. He has NOT mentioned whether it is right or wrong.

/

Amarasiri / March 8, 2016

Gamarala

“It is unfair to blame the President.”

Yes, It is unfair to blame the President, after all he is a Gamarala from Polonnaruwa, still learning finance and investments.

/

Amarasiri / March 11, 2016

President Maithripala Sirisena

RE: MS Takes On Ranil’s Ministry, Calls For Explanation On Sharia Banking After BBS Complaint

Yes, it is quite Diplomatic to give an Explanation on sharia banking, for who who do not know the principles behind it.

The biggest problem, BBS,Buddhists, Three Wheeler Drivers, Taxi Drivers, Shopkeepers, Busgirls, Busboys, and others have with some of these terms, Sharia or Islamic Banking Capitalism, Socialism, etc. is unfamiliarity and ignorance. So Yes, education is needed. This is no big deal, for those who understand this. ( Hello Copernicus, Galileo, Kepler-was a big deal for the Catholic Church, and Galileo Galilei said “The Bible shows the way to go to heaven, not the way the heavens go”-Education.)

The basic principle of Islamic banking is based on risk-sharing which is a component of trade rather than risk-transfer which is seen in conventional banking. Islamic banking introduces concepts such as profit sharing (Mudharabah), safekeeping (Wadiah), joint venture (Musharakah), cost plus (Murabahah), and leasing (Ijar)

Islamic banking and finance

https://en.wikipedia.org/wiki/Islamic_banking_and_finance

The term “Islamic banking” refers to a system of banking or banking activity that is consistent with Islamic law (Shariah) principles and guided by Islamic economics. The contemporary movement of Islamic finance is based on the belief that “all forms of interest are riba and hence prohibited”.[48] In addition, Islamic law prohibits investing in businesses that are considered unlawful, or haraam (such as businesses that sell alcohol or pork, or businesses that produce media such as gossip columns or pornography, which are contrary to Islamic values). Furthermore, the Shariah prohibits what is called “Maysir” and “Gharar”. Maysir is involved in contracts where the ownership of a good depends on the occurrence of a predetermined, uncertain event in the future whereas Gharar describes speculative transactions. Both concepts involve excessive risk and are supposed to foster uncertainty and fraudulent behaviour. Therefore, the use of all conventional derivative instruments is impossible in Islamic banking.[49] In the late 20th century, a number of Islamic banks were created to cater to this particular banking market.

Islamic banking has the same purpose as conventional banking: to make money for the banking institute by lending out capital while adhering to Islamic law. Because Islam forbids simply lending out money at interest, Islamic rules on transactions (known as Fiqh al-Muamalat) have been created to prevent it. The basic principle of Islamic banking is based on risk-sharing which is a component of trade rather than risk-transfer which is seen in conventional banking. Islamic banking introduces concepts such as profit sharing (Mudharabah), safekeeping (Wadiah), joint venture (Musharakah), cost plus (Murabahah), and leasing (Ijar).

Interpretations of Shariah may vary slightly by country. According to Humayon Dar, the Islamic Republic of Iran follows a more liberal interpretation of the Shariah than Malaysia, whose interpretation is more liberal than Turkey or Arab countries. Mohammed Ariff also found less exacting interpretation of Shariah compliance in Iran where the government had decreed “that government borrowing on the basis of a fixed rate of return from the nationalized banking system would not amount to interest and would hence be permissible.”

/

democrat / March 7, 2016

Sharia banking is for muslims there are a number of banks providing sharia banking products the BBS should keep away from this controversy.

/

Amarasiri / March 11, 2016

democrat

“Sharia banking is for muslims there are a number of banks providing sharia banking products the BBS should keep away from this controversy.”

Sharia banking is investment and profit-sharing. and risk-sharing.

The basic principle of Islamic banking is based on risk-sharing which is a component of trade rather than risk-transfer which is seen in conventional banking. Islamic banking introduces concepts such as profit sharing (Mudharabah), safekeeping (Wadiah), joint venture (Musharakah), cost plus (Murabahah), and leasing (Ijar)

It is like investments, and venture capital in a way, except that there s some kind of balance.

Looks like, in Islam, Almighty God, wanted risk and profit to be shared. very democratic and fair, unlike Venture Capital and in Capitalism, where all the people put up the capital is at risk.

/

Plato. / March 7, 2016

Withanage added that Srilanka must not sell its National Identity to Saudi Arabia for US$1 Billion is the last sentence of this piece.

For once Plato is in full agreement with Bodu Bala Sena[BBS].

Srilanka should not sell its National Identity even for US$1 Trillion!

/

Native Vedda / March 8, 2016

Plato.

“For once Plato is in full agreement with Bodu Bala Sena[BBS]. Srilanka should not sell its National Identity even for US$1 Trillion!”

You know I am bit thick.

Could you tell us what this national identity is and why should we preserve it?

/

Adam Ant / March 8, 2016

Excellent question, Native!

Can’t wait for the philosopher’s response!

/

Isreal Lover / March 9, 2016

What are you? Your ethnicity? Do you even live in Sri Lanka?

/

Ajith / March 8, 2016

What a mockery we are in.

What is the identity of Sri Lanka when it come to economy? Is it interest based economy? or profit (just a name change as muslims knows only business and profit :) based economy? What is to do with Identity here.

Is president shows that he is far from capital city of colombo?

/

Gobba / March 8, 2016

But it can sell its women for a much lesser US $ value, not only to Saudi Arabia but to all the Gulf countries. Bravo

/

Indra / March 7, 2016

In the letter I can see that the Kodikara fellow has written the very common Muslim name “Rafeek” in Sinhala as “Raaaaafeek”. Any surprise why this guy is supporting the borubana shit?

/

Amarasiri / March 7, 2016

President Maithripala Sirisena

“President Maithripala Sirisena has called for explanation from the Secretary of the Ministry of National Policy and Economic Affairs M. I. M. Rafeek as to whether the Sharia banking practice is been introduced to the country by following the respective laws and regulations of Sri Lanka.”

Expose, Expose and Expose. Get to the Bottom.

Is Sharia Banking more Efficient than the current Capitalist Banking system and less subject to Fraud>

Compare and Contrast.

What is the Compelling Value Proposition for Sharia Banking, leaving Religion aside?

/

Wow / March 7, 2016

Damn… now what? yahapalanaya has stuck rock bottom. Is there anything we as citizens could do to stop this nonsense? i’m really open to suggestions here.. sharia law or not, the government trying to hold on to power by any means necessary is a serious problem

/

Priyan / March 7, 2016

Don’t worry much folks. Sirisena must be not knowing that this belongs to Ranils Ministry. He is dead scared about pissing off the water boy of West. India wouldn’t order Sirisena to do that just yet.

/

sekara / March 7, 2016

Sri Lanka is one of the few non-Islamic countries to have legislation for the Islamic banking sector. Following amendments to the Banking Act No 30 of 1988 in March 2005, there is now adequate flexibility for conventional banks to establish Islamic banking windows and launch Islamic financial products. (Source: http://www.sundaytimes.lk/071230/FinancialTimes/ft332.html)

Fully fledged Islamic Bank: AMANA BANK PLC

Islamic Banking Windows exist at four Conventional Banks: BANK OF CEYLON, COMMERCIAL BANK OF CEYLON PLC, HATTON NATIONAL BANK PLC, MCB BANK LTD.

There are, besides, Islamic Banking Windows in four Finance and Leasing Companies.

Data as of 27.2.2013

(Source: https://azharseylan.wordpress.com/category/bank-of-ceylon-islamic-banking/)

BBS can think of its own Buddhist Banking and call it Buddhist Banking Systems (It will go well with its own name.)

/

roger / March 8, 2016

this clearly shows the bankruptcy of BBS. Gnanasara became a puswedilla and now this chap has started. What on earth is this MS doing, without knowing what is happening in the country?

/

Goraka / March 7, 2016

If Saudi’s 1 Billion $ is not good enough, ask BBS to provide the financing!

/

Mohamed Ameer / March 7, 2016

Dear Withange,

There is many thing to do in this country. Islamic banking in not a problem for you. if you like take loan or go to other banks.

Now in Sri Lanka there are many killing in roadside ,Why don’t you talk to this matter as you are true Buddhist?

Halal matter is over now and start advice to islamic banking

/

Isreal Lover / March 9, 2016

Why dont you just move to pakistan or ksa. you would love it there! Its 24/7 islam! no pigs, women covered in from head to toe, halal everything

/

Marwan / March 7, 2016

When dealing with most Middle Eastern countries, they will opt for Sharia Banking principles to be applied to safeguard their investments. Western style loans and investments is incompatible and unacceptable to them due to the interest factor which is prohibited in Islam, and therefore is not an option. They would rather deal on profit sharing basis which does not involve a fixed rate of interest.

If we are requesting a loan from them, it is nothing but right that we agree to their terms since they still call the shots. What Dilantha of BBS fame is trying to peddle is to either stop the loan of a billion Dollars from a Muslim nation by referring to it as Sharia (dirty money in his terms), or getting it on our terms (which involves the regular form of repayment involving fixed rate of interest payments). He is again upto his old tricks of arousing fear, hate and anger against Muslims and their Islamic way of living. The more he does it, the more Islam gets its desired exposure and people come to learn, accept and understand the 4eligion of Islam in a whole new perspective.

Interest is defined in the Oxford English Dictionary as, “Money paid for the use of money lent (the principal), or for forbearance of a debt, according to a fixed ratio.”

Actually, individuals and the world as a whole probably know too well the burden of interest, such that no one truly needs the above definition. Interest is something that is known to anyone living in a capitalist country. It has become so completely institutionalized and accepted in modern economies that it is almost impossible to conceive that there are some who completely oppose it and refuse any transactions that involve interest. But there are devout Muslims who refuse to deal in interest.

The actual reason why such Muslims do not deal with interest is that interest has been forbidden by the Islamic religion. At the same time, though, Muslims believe that God’s guidance is based on His knowledge, wisdom and justice. In other words, God does not forbid something from humans for no reason whatsoever. Hence, there are definitely sound reasons, some of which we may be able to clearly recognize, why God has forbidden this practice.

In today’s world, Muslims are constantly being bombarded with arguments in support of dealing with interest. Many Muslims have succumbed to such pressure and supposedly rational arguments, leading them to accept the concept of interest.

The Quran, for example, contains the following verses concerning interest

“O you who have believed, do not consume interest, doubled and multiplied, but fear God that you may be successful. And fear the Fire, which has been prepared for the disbelievers.” (Quran 3:130-131)

This rather strong warning towards the believers warns of a fatal consequence: being thrown into the Hell-fire that has been prepared for the disbelievers.

God also says:

“Those who consume interest cannot stand [on the Day of Resurrection] except as one stands who is being beaten by Satan into insanity. That is because they say, ‘Trade is [just] like interest.’ But God has permitted trade and has forbidden interest. So whoever has received an admonition from his Lord and desists may have what is past, and his affair rests with God. But whoever returns [to dealing in interest or usury], those are the companions of the Fire; they will abide eternally therein. God destroys interest and gives increase for charities. And God does not like every sinning disbeliever.” (Quran 2:275-276)

These verses have many interesting points to them. Commenting on the first portion of the verse, Maudoodi has written,

Just as an insane person, unconstrained by ordinary reason, resorts to all kinds of immoderate acts, so does one who takes interest. He pursues his craze for money as if he were insane. He is heedless of the fact that interest cuts the very roots of human love, brotherhood and fellow-feeling, and undermines the welfare and happiness of human society, and that his enrichment is at the expense of the well-being of many other human beings. This is the state of his “insanity” in this world: since a man will rise in the Hereafter in the same state in which he dies in the present world, he will be resurrected as a lunatic.

Secondly, the verses make it quite clear that there is a difference between legitimate business transactions and interest. The difference between them is so glaring that the verse does not bother to explain them, which is one of the stylistic aspects of the Quran. Thirdly, these verses clearly state that God “destroys interest and gives increase for charities.” This is one of God’s “laws” which humankind cannot necessarily discover on its own. The ultimate and full negative effects of interest on the individual, community and world as a whole in both this life and the Hereafter are known only to God. In fact, perhaps highlighting the meaning of this verse, the Prophet (peace and blessings of God be upon him) also said, “Interest- even it is a large amount- in the end will result in a small amount.” Undoubtedly, in the Hereafter when the individual meets God, all that he amassed via such illegal means will be a source of his own destruction.

Shortly after the above verses, God further says,

“O you who have believed, fear God and give up what remains [due to you] of interest, if you should be believers. And if you do not, then be informed of a war [against you] from God and His Messenger. But if you repent, you may have your principal, [thus] you do no wrong [to others], nor are you wronged.” (Quran 2:278-279)

Who in his right mind would expose himself to a declaration of war from God and His Messenger? Undoubtedly, a stronger threat one will rarely find. At the end of the verse, God makes it very clear why interest is forbidden: it is wrongdoing. The Arabic word for such is dhulm, meaning a person has done wrong to, harmed or oppressed another person or his own soul. This verse demonstrates that interest is not forbidden simply due to some ruling of God without any rationale behind that ruling. Interest is definitely harmful and therefore it has been forbidden.

In addition to the verses of the Quran, the Prophet Muhammad (peace and blessings of God be upon him) also made many statements concerning interest. For example, the following statement clearly demonstrates the gravity of this action:

“Avoid the seven destructive sins: associating partners with God, sorcery, killing a soul which God has forbidden- except through due course of the law, devouring interest, devouring the wealth of orphans, fleeing when the armies meet, and slandering chaste, believing, innocent women.” (al-Bukhari and Muslim)

In fact, another statement of the Prophet (peace and blessings of Allah be upon him) should be sufficient to keep any God-fearing individual completely away from interest. The Prophet (peace and blessings of Allah be upon him) said:

“One coin of interest that is knowingly consumed by a person is worse in God’s sight than thirty-six acts of illegal sexual intercourse.” (al-Tabarani and al-Hakim)

The Companion Jaabir narrated that the Messenger of God (peace and blessings of God be upon him) cursed the one who takes interest, the one who pays interest, the witnesses to it [that is, the interest contracts] and the recorder of it. Then he said, “They are all the same.” (Muslim)

This is a basic principle in Islam. If something is forbidden and wrong, a Muslim should not participate in it or support it in any fashion. Thus, since interest is forbidden, it is also forbidden to be a witness to such contracts, to record them and so on. The Prophet’s words also explain that there is no difference between the one who pays interest and the one who receives it. This is because they are both involved in a despicable practice and, hence, they are equally culpable.

The Prophet Muhammad (peace and blessings of Allah be upon him) also said,

“If illicit sexual relations and interest openly appear in a town, they have opened themselves to the punishment of God.” (al-Tabarani and al-Hakim)

This statement is a reference to one of God’s “societal laws.” The punishment of God may come in different forms in this world or the next.

/

Isreal Lover / March 9, 2016

Hahaha. Are you retarded or have you gone full jihad?

/

Funlover / March 7, 2016

Perhaps we should invite the synthetic pundit on Islam the one and only Izzeth Hoo Insane to contribute his views on Sharia Terrorist Banking. The guy simply loves to open himself wide to get poked by Sinhala Buddhist terrorists.

/

Navin / March 7, 2016

We must be really smart – to have got ourselves such a genius to be our President. Congratulations to us. [Edited out]

/

words / March 8, 2016

Yeah.. toiya smart! :)))

/

Rainzy / March 7, 2016

Sharia banking is said to be better in some aspects, but it will empower the Muslims further.

Are we to have banks on religious lines??

SL destroyed it’s economy, the ‘Sinhala merchants’ and the ‘Southern pioneers’ over some dung-theories, now we are in this state !!

/

Zain / March 7, 2016

Oh dear man, this country is going back to the dark ages. Islamic banking withstood the greatest banking and financial melt down in the history of the world. When the 2007/8 financial crisis hit the world, the US, European, Japanese and other governments had to pumped in trillions of dollars to save their big banks, insurance and mortgage companies from total collapse, and badly avoided a terrible destruction of their entire way of life. Due to this, millions of them lost every thing, their businesses, houses, jobs, cars etc, and still most of them are not fully recovered but the big institutions are fully recovered and back into their same old ways of doing things.

After this incident, when all these governments set up task forces to find out the cause for this crisis and give recommendations to avoid these type of crisis in the future. The experts said, their interest based financial system is a legally set up casino which is gambling the poor depositors money, by this way loosing billions of other people’s money, they were holding gun at their governments and threatening them to bail them out. As they didn’t have much choices, they had to bail out them with the trillions of dollars with terrible pains to their people.

These task forces highly recommended the Islamic banking model, non of these institutions were affected in whatsoever ways by this crisis.

Right now Malaysia is the capital of Islamic banking, and London is the next one. Now, London and Singapore are aggressively promoting Islamic banking into their financial system. In the UK to accommodate this, they are changing old laws and bring new laws as well. Some one known to me, a Sri Lankan origin, US citizen, Islamic banking specialist, was recently brought down to Singapore, all the way from the US providing a thumbing package, by a leading international bank operating there to spear head their Islamic Banking operation.

They are aiming to position themselves to get the big portion of the pie. For now, Islamic Banking and Finance is worth trillions OF dollars and growing rapidly. All those who are banking here not all Muslims but millions of non-Muslims, individuals and business banking are doing it for it’s safety and good concept.

My biggest question is why we have to make big fuss, when it is going to do a great good to the economy? These banks are not only for the Muslims but for any one like the other banks. If one bank with them, they wouldn’t become Muslim but they get good benefit out of them. When the country want to establish an international financial center, these give terrible and utter bad signals to world financial community, who would move their operations when the situation is like this.

London, Singapore and Dubai make huge money and thousands of people are employed in their financial institutions, as all top financial institutions in the world have set up shop in these places, there are many hundred Sri Lankans working there as well.

If this is the attitude of the higher up, I feel sorry for the country, it would move down but not up at all.

/

Marwan / March 7, 2016

Britain is set to become the first non-Muslim country to sell a bond that can be bought by Islamic investors in a bid to encourage massive new investment into the City.

David Cameron will say in a speech on Tuesday at the World Islamic Economic Forum in London that the Treasury is drawing up plans to issue a £200 million Sukuk, a form of debt that complies with Islamic financial law.

The new sharia-compliant gilt will enable Britain to become the first non-Muslim country to tap the growing pool of Islamic investments that is forecast to top £1.3 trillion by next year.

The Prime Minister will say that it would be a “mistake” to miss the opportunity to encourage more Islamic investment in the UK and that the City of London should rival Dubai as a centre for sharia-compliant finance.

“When Islamic finance is growing 50pc faster than traditional banking and when global Islamic investments are set to grow to £1.3 trillion by 2014, we want to make sure a big proportion of that new investment is made here in Britain,” Mr Cameron will tell an audience of senior officials from Islamic countries.

The London Stock Exchange is also preparing to launch an Islamic Market Index to help the managers of sharia-compliant funds identify new investment opportunities.

The UK’s plans to issue its own Sukuk could lead to billions of pounds of British gilts being sold to Islamic investors, enabling the Treasury to diversify away from its traditional sources of funding.

While so much is going on in the outside world, Our BBS Dilantha wants to keep our country and its people like frogs in a well. They neither have the solutions to the problems the country faces, at least a financial system based on Lord Buddhas teachings, but their own forlorn and pitiful Temple life mentality to contend with, with jealousy on the prosperous.

Another large non-Muslim country having Sharia compliant financial instruments is India. As for other countries, you owe it to yourself to go check out why they all claim it to be better than the conventional methods they are used to in methods of financing.

/

Jayagath Perera / March 7, 2016

Permit me to qoute a part of your article as follows:

“Sirisena’s Additional Secretary, S. T. Kodikara, in a letter addressed to Rafeek has called for explanation within two weeks on the matter.”

But the letter says in Sinhala as follows:

“පවත්නා නීති හා විධිවිධාන යටතේ එවැනි ක්රියාමාර්ගයක් ඔබ අමාත්යාංශය ගෙන තිබේද යන්න පිළිපබඳව සති 02 ක් තුළ මා දැනුවත් කරන මෙන් කාරුණිකව ඉල්ලා සිටිමි.”

Now if I translate the Sinhala text above into English is as follows:

“You are kindly requested to apprise me within two weeks whether your ministry has taken such an action within the existing laws and regulations (include rules, directions etc.). “

Now that is not calling for explanations. One Dilantha Withanage has apparently met the President and handed over some letters making representations on a matter. It is nothing but fair by everybody for the Secretary to the President to obtain information on this matter without any delay from the line Ministry concerned. In my view, since a mountain can be made out of a mole hill to create disunity in the country, the requisite information should have been submitted within 24 hours. The country cannot afford another racial / ethnic / religious disturbances.

I must also let it be known that if explanations are to be called then the letter would have been signed by the Secretary to the President himself stating that the President has directed him to do so and it would not be with that polite ending.

I my self have no regard for BBS but as the President of the country, President Sirisena should give a fair hearing to any group however odious they may be and quickly verify the representations made through the line Ministry.

/

Mallaiyuran / March 8, 2016

If no China there is Saudi. If no Saudi there North Korea!

We all ways new new ways to do third grade dealings.

If there any of the $18 billions is in Saudi, they have to give that money free, not as loan.

/

K.A Sumanasekera / March 8, 2016

Singapore Mahendran gives Shria law to Whabis for the USD 1 Billion from Saudia.

What did Galleon give to Vellalas for the USD 1 Billion from Diaspora?…

/

Jehan / March 8, 2016

We must not be led by BBS fools, who are hiding under the saffron robe to create another

Stupid non-issue.

Take for instance the Hallal issue: In SL there is no Hallal label , for Sri LAnken manufactured food products,

Therefore most Muslims avoided the SL product, buy the imported Hallal certified product, who is loosing.

Though for exports the same product has HAllal certificate.

Sri Lanka had the opportunity to be the certified Hallal supplier of choice, if not for the Balu senna and Gota policies,

This business is a 300 billion business, how many people we could have employed of all communities.instead of sending our women to work in the Middle East.

Loss of income due to less tourist coming from Middle East, because of Bbs nonsense and HAlal issues,

Thailand has a 10 billion Hallal certification industry and a million Muslim tourist from Middle East.

Japan has come up with a Muslim tourist initiative.

Why not Sri Lanka, are we to be led by jack ass bbs policies, who is the dumb fool withanage, for him to be given

Guranteed by the central bank governor.

With less than 4000 votes, I don’t think they have any policies, except talking crap,

Gnanasara the dumb ass should be in jail for aluthgama .

We need our country back, be it Buddhist/Christian/Hindu or Muslims, we are Sri lankens,

We kicked out the jack ass MS and family, we don’t need the tail to wag the dog.

/

God / March 8, 2016

I would rather borrow from Saudi Arabia than the likes of IMF.

/

Mohamed / March 8, 2016

This is the most funny news I heard in this century.

In fact Saudi and naming the interest as profit in wording and play then name of shaira bank.

The President of Sri Lanka has neither knowledge nor consultation than just believing what BBS believe and act foolishly.

Simply President, BBS and Saudi which demand so, all of them are in the same bucket of ignorance of what they stand for. Shame on them for their knowledge and inability to have minimum consultation before action.

/

Mohamed / March 8, 2016

Sharia banking brand in Sri Lanka is nothing but a back door entry mode to some religious dignitaries in to a job market (Boards of Banks) showing muslims as market and they can promote to be customers in religious ground.

In order to address this, we need academic contribution to say both this is just a banking with different brand vs if at all what change it can bring to economy.

Instead politicizing this by a government itself shows our academic immaturity to address beyond foolishness and how irresponsible we are.

/

Zain / March 8, 2016

Our prophet(PBUH)said, when one ask money, see that he could pay it back, if not give him some money and forget it for good. Also he said, if one give money to another, even if he stands on his shadow, that too amounts to usury – interest. It shows, how much Islam is against to taking and giving interest. All the ills of modern world economy is due to it’s interest based system. It’s a real vicious cycle which wouldn’t allow one to raise his head, and lead a good life.

/

arjuna / March 8, 2016

and your Prophet said , charge interest from non Muslims an give it to Muslims , breed like rats and take over the country, produce and deal drugs to non Muslims, marry 4 wives and breed , lie to non Muslims to get the benefits for Muslims , on and on..

/

Isreal Lover / March 9, 2016

Cant wait till sri lanka has its own draw muhammed day!

/

BBS Rep / March 8, 2016

Withanage says “irreparable damage to social cohesion and integration of different communities into mainstream society.”

Now, now, now, look who is talking about integration of different communities and social cohesion. Withanage you your BBS are a humbug.

/

colin / March 8, 2016

If we can get back the 1 billion dollars stacked away in Dubai by you know whom then we may not need the i billion dollars from the Sharia Bank of Saudi Arabia,

I hope Withanage will also scream out in the same breath .that we must ban all Sri Lankans (especially the majority community who comprises over 75 percent) from working in the Muslim countries of the Middle-East and try and bring back those falling into that category.He wouldnt dare do so.

/

Dr.Rajasingham Narendran / March 8, 2016

I have worked in Saudi Arabia for 30+

/

Dr.Rajasingham Narendran / March 8, 2016

I have lived in Saudi Arabia for 30+ years. Islamic banking involves a service charge on loans, which is in monetary terms equivalent to the interest rates charged by non-Islamic banks that operate in other countries. From what I understand Sharia condemns Usury, which is charging unconscionable rates of interest. In regulated banks this not happen.

Further, the banks operating in Saudi Arabia pay a ‘ Profit’ on deposits. This is competitive and compares with the interest earned on deposits in non-islamic banks elsewhere.

Islamic banking has been operational in Sri Lanka for a long time. many commentators here have also pointed this out.

Much ado about nothing!

Do those working for the president know how to get information on such matters from a Google search? why should the president respond to mischief making by the BBS? Mr.President, you have better and more important things to do. Your Yahapalanaya is leaking and developing more leaks by the day. Request the PM to sack the Higher Education and Education ministers. They should not hold their assigned portfolios a day longer! Give the leadership of the SLFP and the UPFA to someone you can trust. You are compromising on the promises you made to the electorate because you are pandering to the unreasonable demands of the political formations you lead. They sabotaged the 19th and 20th amendments. They have also started playing word games with the proposed new constitution. Isn’t it supposed to be a new constitution? Why pretend otherwise? Are you and the government you lead trying to make us idiots once again?

Dr.Rajasingham Narendran

/

Patriot / March 8, 2016

An eye opener for idiotic president!

/

Upul / March 8, 2016

Morons!

Saudi money is good. Islamic banking with no exhorbitant interest and stringent rules no good!

Curious to know how many non-muslims are using the so-caled Islamic banking standards?

Same racket like the Halal episode. No body was forced to eat it, to begin with. Why are the taverns closed on Poya days? Is it to prevent the Muslims from drinking?

/

Gune / March 8, 2016

Don’t take the BBS seriously. We cannot run a country on the whims and fancy of the BBS who act in direct contravention of the teachings of Budhism. They are a rogue organization funded by the west to create destability and need to be taken to severe task.

/