By W A Wijewardena –

Dr. W.A Wijewardena

The case of a bankrupt company

What do you think of a private company which is indebted to the hilt, does not earn enough to repay its debt and experiences a low sales growth which is declining year after year? Surely, it is a problem company needing quick fixing. If its capital has completely been eaten up, it is said to be a bankrupt company which, as those in the market would say, is in the red. To convert it into green, capital has to be brought in from outside, while its operations are restructured. If this is not done, the private company will go under and has to stop operations before the authorities would force it to close shops.

Sri Lanka incorporated: fast moving toward bankruptcy?

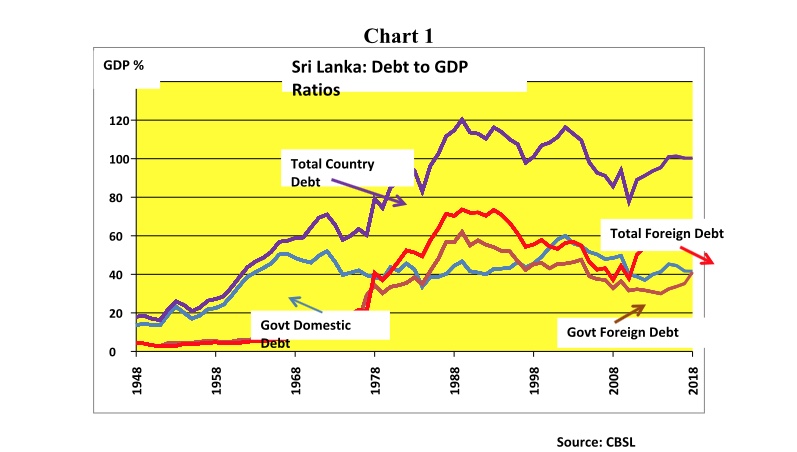

Now consider the parallel between this company and the country called the Democratic Socialist Republic of Sri Lanka. The total public debt incurred by its central government is about 83% of the country’s total output, known as the Gross Domestic Product or GDP. When the central government’s borrowings from the Central Bank and state banks are also added, the total debt increases to 85% of GDP. That number includes only the foreign borrowings of the central government. In addition, private sector entities also have made foreign borrowings amounting to some US $ 21 billion.

When that number is also added to the central government borrowings to represent the total country borrowings, it rises to 100% of GDP in 2018. Sri Lanka was able to reduce the share of these borrowings from a peak of 116% of GDP in 2002 to 77% in 2010. This is shown in Chart 1. But since then, they have been rising ominously mainly due to the increases in foreign debt contracted by both the central government and the private sector.

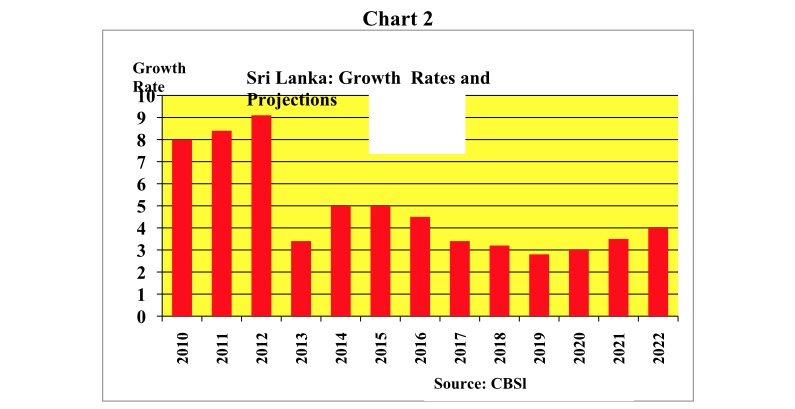

To complicate the ominous economic situation, economic growth has been falling continuously from 9% in 2012 to 3% in 2018. The growth projections for 2019 have been even below 3% with no hope of economic recovery during the next 3 year period, as shown in Chart 2.

Expanding the debt profile in a slow real growth era

Unlike a private company in a similar situation, Sri Lanka is not yet a bankrupt country that should go into compulsory liquidation.

With its single digit inflation of around 4%, its government can still repay domestic debt by either borrowing from the domestic economy or by printing new money. The country can still access foreign commercial markets to raise foreign exchange funds to repay its foreign debt. However, the country’s debt profile is changing for the worse year after year pushing it to the edge. Presently, annual debt repayment obligations are almost equal to the total government revenue. In the next few years, it will exceed the revenue levels making it necessary for the country to borrow in larger volumes and repay its debt.

This debt recycling has a limit since no country can continue to expand its debt profile unless it has comfortable real economic growth to back such borrowings. In this connection, the danger signs have already been shown by the low economic growth in the recent past with no prospect for economic recovery in the next few years. Hence, though it may not be fully bankrupt today, it is pretty much on the way to bankruptcy.

Hence, without further borrowing, the country cannot maintain its unblemished track record of meeting all foreign debt obligations in time. The casualties in this backdrop are ever-rising foreign debt, depleted foreign reserves, falling exchange rate, stalling economic growth and finally accelerating inflation.

The blame-game should stop forthwith

Hence, the ominous debt profile is the public enemy number one looming over Sri Lankans today. The two major political players who have shared the political power in the country since independence have been on a ‘blame game’ accusing each other for the critical state in the country.

The most commonly used debt-burden indicator is the amount of public debt falling on a single individual in the country, a figure derived by dividing the total public debt by the total number of people in the country. By quoting this number, they are in the habit of awarding a clean certificate to themselves, while accusing their political rivals.

However, if any political party is desirous of earning this clean certificate, there is a fundamental qualification which it should have acquired. That is, when that political party had been in power, the government budgets its Finance Ministers had presented should have been either balanced budgets or surplus budgets. If they had been balanced budgets, they do not add new debt to the debt profile. If they had been surplus budgets, they have indeed repaid some of the previous debt thereby contributing to shrinkage of the total debt.

The bold example by M D H Jayawardena

In this respect, there is only one Finance Minister in the whole of the post-independence history who can claim that he has not added debt burden on the people. That was M D H Jayawardena who held the Finance Portfolio during 1954 to 1956. In his budgets of 1954 and 1955, he had surplus budgets of 0.5% and 2.2% of GDP, respectively.

The macroeconomic achievements during this short period were for the better. The total public debt fell from 27% of GDP in 1953 to 21% by 1955. Government’s borrowings from the Central Bank and commercial banks on a net basis, that is, after setting off government deposits from borrowings, declined from Rs 455 million in 1953 to Rs 186 million in 1955. The beneficial effects on inflation and economic growth were remarkable during this period. Inflation rate, measured in terms of the Colombo Consumers’ Price Index, fell from 1.6% in 1953 to a negative 0.5-0.6% in 1954 and 1955 and continued to be in the negative range even in 1956 before accelerating to 2.6% in 1957.

Economic growth accelerated from 2% in 1953 to 6% in 1955. In the subsequent 4 year period, growth fell again on average to 1.6% per annum. Sri Lanka had a comfortable surplus in the balance of payments or BOP amounting to about US$ 60 million in each of the two years. Since then, Sri Lanka’s BOP turned to be negative, depleting foreign reserves, putting pressure on the fixed exchange rate to be devalued by the government and forcing the authorities to impose the most stringent import and exchange controls on the citizens. Thus, all Finance Ministers, except M D H Jayawardena, are guilty of the present sad state of debt overhang in the country.

Proposing to settle debt by borrowing more

The leading candidates contesting the forthcoming Presidential Election of 2019 have expressed their anger at the overhanging debt problem in the country.

However, the solutions they have suggested pose two issues. One issue relates to the strategy of borrowing funds from a cheaper source and repaying the existing foreign debt. Such an approach can be applied only in the case of the maturing debt owed by the government and not by the private sector borrowers. This is because the early repayment of the entire debt portfolio would require elaborate negotiations with creditors and, in most cases, a payment of a penalty.

Sri Lanka’s private sector also owes some US$ 21 billion to diverse creditors and any early repayment arrangement has to be made by individual borrowers having negotiated with individual creditors. A President representing a country cannot do this. It is worthwhile to note that, with regard to the maturing debt, this approach suggested by some of the key Presidential candidates is exactly similar to the debt recycling being done by government debt authorities.

What is ignored by all the parties is that it does not take the country out of debt. It simply make the country more indebted trapping it in a bigger debt burden, since it now has to borrow money even for paying interest on the existing debt. Hence, this solution is similar to the proverbial saying in Sinhala ‘making the chair by dismantling the barn’.

Debt should be repaid via real sacrifices

The second issue arises from a misunderstanding that a country can get out of debt without making a real sacrifice. Though debt is denominated in money form, it is not money that is lent. A lender has to save a part of his real earnings to give out as a loan by sacrificing his current consumption in favour of consumption to be made in the future. For instance, if I borrow one rupee, I do not simply borrow it in money form. The person who lent me that one rupee has to sacrifice his real consumption equal to one rupee. When that one rupee is transferred to me, I have the ability to command over a basket of real goods and services worth of one rupee. Hence, when I repay it and pay interest on it, I transfer to my creditor a basket of real goods and services worth of one rupee and the interest component applicable to it. Hence, debt repayments are not mere financial repayments but transfers of real goods and services to creditors by borrowers. The political leaders appear to be in the belief that they can take a country out of debt simply by making only a financial transfer.

The weird story of an African country solving its debt problem

Apparently, this view that debt could be settled by mere financial transfers has arisen from a a story that has gone viral in the social media about a country getting out of debt simply by using a hundred dollar bill paid as advance to a hotel clerk for occupying a room in that hotel. The story in question is as follows.

An American tourist comes to an anonymous African country where people are indebted to each other. When the American asks for a room in the only hotel in the country, the receptionist insists that he should pay an advance of US$ 100. The tourist who hands a hundred-dollar bill to the receptionist hangs around in the lobby until the room is ready for him. The receptionist uses the hundred dollar bill to settle the hotel’s debt to the butcher; butcher to settle debt to his daughter’s tuition master, the tuition master to a gold smith, gold smith to a prostitute and so on. Finally, the prostitute comes to the hotel with the hundred dollar bill and pays the receptionist to buy a beer from the hotel. The tourist who is not satisfied about the quality of the room refuses to stay there and asks for the advance he has paid. The receptionist who now has the hundred dollar bill promptly returns the advance. But by that time, all the people in the country have now settled all their debt and are ready for a new beginning.

The suggestion that the Central Bank should print money and repay government debt

Having been enamoured by this story, a senior politician suggested to me that Sri Lanka government can settle all its domestic debt if the Central Bank prints Rs 1 trillion and lends to the government. After the government has paid all its debt, the Central Bank can adopt a tight monetary policy and take that money back to prevent it from causing inflation. I told him that the story has two defects. One is that it still has the issue of how the government will repay its debt to the Central Bank. The other is its wrong assumption that debt can be settled permanently by the transfer of mere financial funds to creditors. That should come from sacrificing real resources in favour of the government by way of taxes. That is why in good olden days people paid taxes to kings in real goods. But, this is a painful affair and for a country ridden with mounting debt, there is no any other option available.

The way-out is only by real sacrifices

Thus, the Presidential hopefuls intent on resolving the country’s debt problem permanently should follow only one policy option. That is to run a surplus in the budget, as was done by M D H Jayawardena in 1954 and 1955, and start repaying the existing debt. But, this will address only the domestic debt of the government. About the foreign debt owed by both the government and the private sector the proper course is to strengthen the country’s foreign exchange earning capacity by promoting export of merchandise goods and services.

Any other measure done will simply be a temporary palliative that would worsen the country’s conditions in the long run.

*The writer, a former Deputy Governor of the Central Bank of Sri Lanka, can be reached at waw1949@gmail.com

Nosey Parker / October 14, 2019

Dr . Wijewardena

Thank you for your very interesting, but rather alarming article. What precautions, if any , should ordinary citizens take , to protect themselves when the proverbial ‘s..t eventually hits the fan’ ?

/

Don Stanley / October 14, 2019

IMF and World Bank generate fictional debt and GDP figures to advance Washington’s agenda and trap so called Middle Income Countries by putting them into the Middle Income Country (MIC) DEBT TRAP!

ha, ha, ha!

Like the previous HIPC initiative of IMF to trap poor countries to carry liabilities and asset strip them which was refused by all which nearly put the IMF out of work.

Now, How did World Bank come up with pure fiction that Sri Lanka became an UPPER Middle Income County last month when after the Easter Disaster Sri Lanka became a Lower Middle Income Country? This was to force signing of the Washington MCC land grab and military bases project in Sri Lanka…

But did a single Economist from IPS or the University challenge the WB fictional classification of SL as an upper MIC????! Dr. Wijewardene why don’t you challenge the WB to explain itself for putting out fake debt and GDP figures?

/

ramona therese fernando / October 14, 2019

Yes, run a surplus on the budget and bring in the Austrity measures. But as this will impact goods and services, tax the Oligarchs (Kletocrats in Sri Lanka…. they didn’t create a thing- just destroyed the land and force-worked the people). And country shouldn’t listen to Coomaraswamy telling us to buy cheap money from India.

/

ramona therese fernando / October 14, 2019

Austerity*

/

ramona therese fernando / October 20, 2019

Kleptocrats*

/

Kalupahana / October 14, 2019

Dr. Wije: The Washington Consensus and its fake development “experts and advisors” which debt traps countries all over the world has worked hand in hand with corrupt and financially illiterate politicians from the UNP and SLFP to bankrupt Sri Lanka and capture Lanka’s POLICY SPACE. This is what MCC has done messing around for the past 10 years with Bondscame Ranil and US citizens Rajapaksas.

Intellectually bankrupt local economists and think tanks have contributed to the Foreign fake aid induced development Debt trap and development debacle in Lanka.

However, Sri Lanka is a goldmine given its extensive marine resources, both living and non-living and geostrategic location.

If Greenland which Trump wants to buy is worth a trillion $ because of its mineral weatlth Sri Lanka is worth more! also given its Geostrategic location in the Indian Ocean. This is why Washington Consensus together with MCC fake advisors in Bondscam Ranil’s office have worked to bankrupt and asset strip Sri Lanka to set up military bases, cheap. This is the real reas

/

chiv / October 14, 2019

Over to you Prof.Milton Rajaratna of “Lanka School of Economics and Politicking”. Question, the talk/thought on bankruptcy always reminds the US /West or World Bank to some Lankans. One of the graph / Chart shows our plight and mismanagement since independence. Was US and World Bank responsible then ??????

/

Yahapalanaya / October 14, 2019

The country’s IRD should be going after and taxing the top 5% of earners at a reasonable rate and do away with some unfair tax benefits which are draining the country’s economy. Most of top 5% are receiving tax benefits (Ex. Fuel allowance, permits) and if these benefits are leading to any savings that can be reinvested into the local economy then that is good for the country. But what these 5% majority are doing is that most of these savings are consumed for the purpose of going on foreign trips spending overseas which is of no use to local economy.

/

Mallaiyuran / October 16, 2019

Dr.Wijayawardane’s Hotel story is interesting. But the end seems to be in pretty difficult destitute. Loans seem to be settled locally. But the tourist has rejected the room. Hotel is in bad shape. It needs repairs before it can take any further advances from potential customers, who book the room. Where the loan for the repair going to come? Where the new income going to come for the new start?

The solution for Lankawe is, possibly, available with Anura.

1). Stop all the commission payment to senior official and politicians. Then the budget will balance, without citizens cutting consumptions.

2). Bring back all the foreign Bank deposits from all the politicians. This will be more than enough to pay government’s external loans and spend a few bucks on new investments too.

Anura Is saying that they are holding the people’s money and those all have to be repossessed.

But the main to parties who looted all institutions keeping silent on that hoping one day civilians will have to cut the consumption and settle the loans.

/

JD / October 19, 2019

Dr. Wjiewardane’s Bar graph about srilanka’s GR -projections explains every thing. Because of the peace dividend, Sri lanka had a growth until 2012. Mahinda Rajapakse and his Honchos did not know what to do raise that after that. Instead, he closed textile mills that R Pemadasa set up. All his big expenditure was to increase his amount of foreign held assets.

Ranil or his honchos including Mangala are the same. See in the photo how Mangala the Lingerie designer has become a Financial expert and the Expert Ajith Kumaraswami seems bored and depressed.

Govts since 1980 printed currency almost every every year and they did not keep any trails about what was happening to those money. I hear ever now, Lot of Sri lankan money is held outside the country. That may be the reason why Mangala has to issue rupee T bills and sell those to those who trade with american dollars.

USA boasts they are a very rich country. Yet, they are self sufficient in their staple food – wheat and. Meat. Sri lanka was doing agriculture since the times unknown. Yet, they do not know how to be self sufficient in food.

How old is the IMF and world bank. and what are the country who have become developed because of IMF or WB.

/