By D.N. Raththepitiya and K.T.T. Dasunpriya –

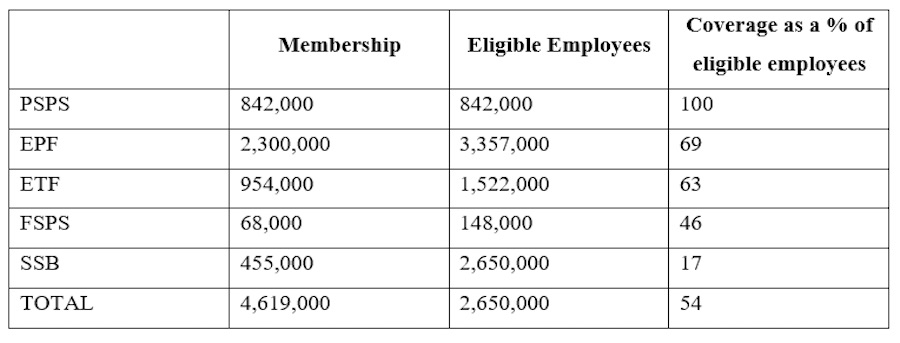

Analysis of the existing coverage for formal and informal workers indicate that whilst the mandatory pension schemes for workers in the formal sector has a coverage rate of approximately 75%, participation of workers in the informal sector in voluntary retirement schemes is poor i.e. 34% coverage.[1] Low coverage of workers in the informal sector of the country in retirement benefit schemes is a problem as it will result in these employees experiencing high levels of poverty in their retirement.[2] These high levels of poverty are likely to intensify with age.[3] High poverty amongst the older demographics is likely to place a significant economic burden on the country, as the state would have to step-in to meet the food, shelter, and other basic needs of individuals in this demography. This in turn will undermine socioeconomic development in the country, as vital financial and other resources would have to be deployed to support the basic needs of these individuals. Part of the reason for low coverage of workers in the informal sector in retirement benefit schemes can be attributed to the fact that the legal framework for retirement benefit schemes for workers in the informal sector is different to that of workers in the formal sector. For example, as stated previously employee contribution to retire schemes is mandatory in the formal sector, whilst it is not mandatory in the informal sector. This study has been undertaken to determine if the current legal framework in the retirement schemes for informal workers is the reason for this low coverage.

Negombo fish seller | Picture by Dr. Nirmal Ranjith Dewasiri

Retirement benefit schemes in Sri Lanka can be broadly segmented into mandatory and voluntary retirement benefit schemes. Out of these two schemes, retirement schemes are mandatory participatory schemes for workers in the formal sector and voluntary participatory schemes for workers in the informal sector. Mandatory retirement schemes for formal workers include Public Service Pension Scheme (PSPS), the Widows and Orphans (W&OP) scheme, the Public Service Provident Fund (PSPF), and the Employees Provident Fund (EPF). Voluntary contributory retirement benefit schemes include the Farmers’ Pension and Social Security Benefits Scheme (FPS), Fisherman’s Pension Scheme (FSPS), and the Social Security Board (SSB). In addition to these mandatory and voluntary retirement benefit schemes operated by state organizations, there are also a number of voluntary retirement benefit schemes operated by private firms in Sri Lanka. These schemes include medical insurance scheme, pension schemes, and annuity payments. Key private firms offering retirement benefit schemes include insurance companies and commercial banks in the country

Retirement benefit schemes are important for both workers and society for a number of reasons. Retirement benefit schemes are important for workers as it enables workers to retire at a certain age, protects their income and living standards, and enables them to live a healthy and active life post retirement.[4] This importance of retirement benefit schemes is evidenced by empirical research which shows a growing percentage of Sri Lanka’s elderly population sliding into poverty due to the lack of sufficient replacement of pre-retirement income. This lack of sufficient replacement of pre-retirement income can be attributed to the low percentage of the population covered by retirement benefit schemes and weaknesses in the existing retirement benefit schemes i.e. decline in purchasing power due to inflation. Retirement benefits schemes are also important for society, as it reduces its financial burden i.e. high financial independence of retirees reduces the need for society to allocate financial, health, and other resources to support this demographic. For example, low percentage of the population covered by retirement benefit schemes has forced the Sri Lankan Government to allocate significant resources in subsidizing housing and health needs of the elderly.

Snapshot of the main characteristics of primary retirement benefits schemes in Sri Lanka

Current coverage of formal and informal retirement benefit schemes[5]

Discussion

Discussion of the legal framework for FSP

Findings from the doctrinal research revealed that a number of statutes have been introduced relating to voluntary retirement benefit schemes for workers in small scale enterprises. ‘Farmers’ Pension and Social Security Benefit Scheme Act No.12 of 1987’ was introduced as legislation for the establishment of a pension scheme for individuals either directly or indirectly engaged in the agriculture sector of Sri Lanka. The primary objective of the state in introducing this legislation was to provide social security for workers in the agriculture industry during their retirement and reduce their dependence of state welfare and family support after retirement[6]. The individuals in Sri Lanka community eligible to enroll in this scheme is clearly stated in No.452/7, Gazette 7 Gazette of May 1987. As per this Gazette in order to qualify for the scheme, an individual has to be a cultivator, whether as an owner, lessee, or tenantcultivator and should be engaged in the cultivation of either paddy or other types of cereals, vegetables, subsidiary crop cultivations, cultivation of other field crops, cultivation of betel, fruits and sugar cane, and cultivation of tuber and roots crops. Further, this Gazette also provides provision for owners, lessees, and tenant-cultivators to join the scheme if they are certified as farmers by an authorized officer under the Agrarian Service Act, No.58 of 1979, the Land Development Ordinance (Chapter 464), or the Crown Land Ordinance (Chapter 464). Those in the agriculture sector eligible to join this scheme was further expanded under Gazette No.522/6 of 7 September 1988. Under this Gazette, individuals employed in livestock farming, those whose primary livelihood is animal husbandry, and laborers employed in livestock farming, animal husbandry and agriculture crop cultivation are also eligible to join the Farmers Pension and Social Benefit Scheme. Further, legislation limits eligibility to enter this scheme to owner cultivators where the total farm land extent does not exceed 10 acres. Note, the land extent not exceedin10 acres includes farm land holdings of both the owner and his or her spouse. Further, in order to be eligible, individuals should not be members of any other formal or informal retirement benefit scheme in the country, and should be not less than 18 years in age and not more than 59 years of age. The Farmers’ Pension and Social Security Benefit Scheme Act No.12 of 1987 states that the rate of contribution to the scheme and subsequent amendments to it be specified by government gazette. Further, under this scheme whilst the minimum contribution should be according to rate of contribution stipulated by the government, there is no upper ceiling on the contribution i.e. members can contribute more than the stipulated contribution if they so wish. Further, the amount and the number of contributions that have to make by each member is decided by the AAIB based on the age of the member at the time of enrolment in the scheme. Members of this scheme have the flexibility of either making regular period payments to the scheme until they reach the vesting age, or have the flexibility of making a one-off payment in the year on enrolment with no subsequent or additional payments. Member making one-off payments are eligible to a discount on the total amount payable. The discount rate in this regard can is decided annually by the AAIB. Regular payments to the scheme can be made by member either annually or bi-annually[7]49

All payments made by members to the Farmers’ Pension and Social Security Benefit Scheme is recorded in a passbook which is issued at the time the first regular payment is made to the scheme. Members are required to ensure that all payments made to the scheme are recorded in this book. Members are required to handover the passbook at the vesting age i.e. 60 years, or whenever he or she is entitled to draw the pension. Members can obtain a new passbook in the event the passbook is lost through the nominal payment of Rs.25. Members who make a one-time payment are not issued with a passbook as they do not make annual or bi-annual payments. Records of member payments are maintained at the AAIB District Office with a copy of records been maintained by AAIB Head Office[8] . Under the Farmers’ Pension and Social Security Benefit Scheme Act No.12 of 1987, members who make the stipulated payment for the stipulated period of time are entitled to a monthly pension upon reaching the vesting age. Further, members who have made at least 75% of the total amount stipulated are eligible for reduced pension. Members who contribute more than 10% but less than 75% of the stipulated amount are provided a refund. This refund comprises of the full amount deposited to the scheme along with accumulated interest upon reaching the vesting age. Members who contribute less than 10% of the stipulated amount are not provided a refund. The Farmers’ Pension and Social Security Benefit Scheme Act No.12 of 1987 also includes legislation relating to survivor benefits for members of the scheme. Survivor benefits enable the legal heir of the deceased member to claim the net contributions made to the scheme plus any accumulated interest within a one year period. A special gazette introduced social security benefit schemes for members of the Farmers’ Pension and Social Security Benefit Scheme between the ages of 18 to 54 years.[9] This Gazette resulted in.

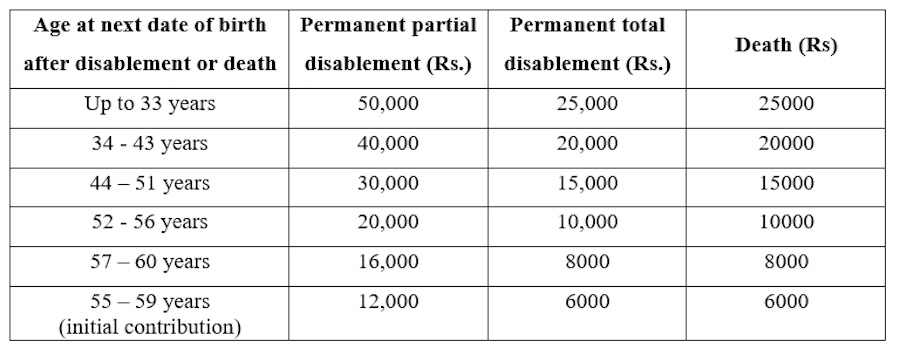

farmers joining the scheme between the ages of 55 to 59 years not been eligible for the social security benefits provided by the scheme. This limitation was addressed in new gazette which was issued in 1988 which included farmers joining the scheme between the age of 55 to 59 years in the social security benefits of the scheme[10] . Under survivor benefits scheme, the legal heirs of a deceased member between the age of 18 year to 59 years, or members between the ages of 54 to 55 years are is entitled to claim all contributions made by the deceased member to the scheme plus any accrued interest within one year of the death. In the event the member has died after the vesting age, legal heir are entitled to claim all contributions made by the deceased member plus any accrued interest, minus all retirement benefit payments made to the member before death.[11] The social security scheme introduced under Gazette No.452/12 of May 7, 1987 comprises of a disability benefit, disablement gratuity and death gratuity. The social security benefits are funded by a separate social security benefit fund established under Gazette No.452/12 of May, 1987. This social security benefit fund is funded by annual contribution of Rs.60 from all members which is deducted from their annual contribution. Shortfalls in the funding of the account are subsidized by the state. The disability benefit stated under Gazette No.452/12 of May, 1987 relating to Farmers’ Pension and Social Security Benefit Scheme Act No.12 of 1987, comprises of a permanent and partial disablement benefit, and a permanent and total disablement benefit. Permanent and partial disablement benefit includes loss of sight in one eye, loss or permanent disability in one hand or one leg. In the event of disablement, the member has two benefit options. In the first option, the member can claim the disablement benefit of Rs.25,000 plus the full contribution made to the retirement benefit scheme at that point and any accumulated interest, and leave the scheme. In the second option, the member has the option of not claiming the disablement benefit, and receiving a pension at the vesting age[12] . Members claiming permanent and total disablement benefits under the social benefit scheme of the Farmers’ Pension and Social Security Benefit Scheme Act No.12 of 1987 need to have suffered sickness or illnesses detailed in Gazette No.452/12 of 1987. Similar to the partial disablement benefit scheme, the permanent disablement benefit scheme allows permanently disabled members to withdraw the total permanent disablement benefit of Rs.50,000, plus all monies contributed to the retirement scheme, and accumulated interest from these contributions and leave the scheme, or the member cannot claim the permanent disablement benefit and receive a pension at the age of 60 years[13] . Death gratuity scheme introduced under Gazette No.452/12 of 1987 relating to Farmers’ Pension and Social Security Benefit Scheme covers all members with a death gratuity. Under this death gratuity, the legal heirs of the member are entitled to death gratuity benefit in the event of the member’s death before the vesting age. Death gratuity payments range from Rs.6,000 to Rs.25,000 based on the age of the member. In addition to the death gratuity benefit, legal heirs of the deceased member are also entitled to claim all contributions made to the retirement scheme plus any interest which has accumulated from these contributions. Gratuity payment entitlements for partial disablement, permanent disablement, and death of members are detailed in the below table[14].

Legal framework for FSPS

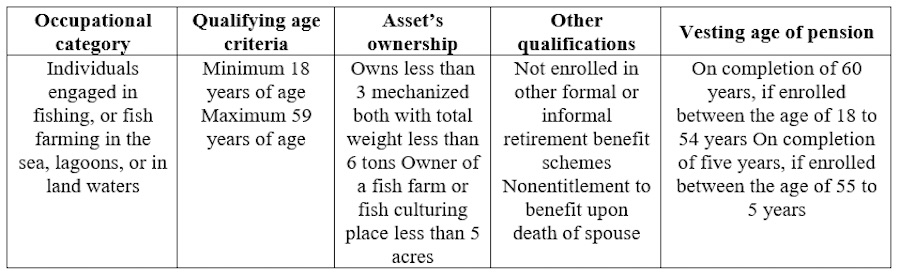

A pension and benefit scheme similar to the pension and benefit scheme for farmers has also be established in Sri Lanka. The pension and benefit scheme for fisherman was established in the country under the Fishermen’s Pension and Social Security Benefit Act, No. 23 of 1990. Under this legislation, fishermen in the country between the age of 18 to 59 years are eligible to join the Fishermen’s Pension and Social Security Benefit. Note, fishermen in this act are defined as ‘those engaged in fishing or fish farming, either in the sea, lagoon, or inland waters’. The eligible criteria for those individuals who quality as fisherman under the previous definition under the Fishermen’s Pension and Social Security Benefit Act, No. 23 of 1990 are detailed in the below table

Qualification criteria for the Fishermen’s Pension and Social Security Benefit Scheme

Similar to the Farmers’ Pension and Social Security Benefit Scheme Act No.12 of 1987’, the Fishermen’s Pension and Social Security Benefit Act, No. 23 of 1990, also provides two options for members to make payment i.e. regular annual payments or a one off payment. Members making one-off payments are provided with a discount which is decided annually by the AAIB. Further, members wishing to make one-off payments to the scheme are permitted to make the payment in two or four equal instalments within 12months of enrolling in the scheme.[15] However, unlikely the farmers’ pension and benefit scheme where members are permitted to make the annual payment in two instalments, members of the Fishermen’s pension and social security benefit scheme can make the annual payments in four payments[16] Annual contribution of a member in the Fishermen’s Pension and Social Security Benefit Scheme is determined based on the age of the member at the time of enrolling in the scheme. Contribution rate to the fishermen’s pension and benefit scheme is established by gazette and is also amended by gazette[17] Annual contribution rates is determined at the time the individual joins the scheme, and is based on the age of the individual at the time of joining the scheme. Age based calculation of the annual contribution has resulted in the scheme having a lower financial impact on younger members of the fishing community in comparison to older members. Pension entitlement scheme in the Fishermen’s Pension and Social Security Benefit Scheme is similar to pension entitlement in the Farmers’ Pension and Social Security Scheme[18]. Members who make more than 75% of the stipulated contribution are entitled to receiving a full pension on completion of 60 years, Members who contribute more than 10% but less than 75% of the stipulated contribution are entitled to refund. This refund comprises of the total amount contributed by the member to the fund, plus interest accumulated on this contribution. Members whose total contribution is less than 10% of the stipulated amount are not entitled to any refund. Members who joining the scheme between the ages of 55 to 59 years are entitled to a pension upon completion of five years of payments.

Survivor benefits outlined in the fisherman’s pension and social benefit scheme are similar to the survivor benefits detailed in the farmer’s pension and social benefit scheme, as this scheme also offers disablement benefits, social gratuity and death gratuity.[19] A key difference in the survivor benefits for legal heirs of family members in the Fishermen’s pension and benefit scheme, and the Farmers’ pension and benefit scheme is that the fishermen’s scheme, permits the spouse of the deceased member who do not claim the lump sum benefit, to receive the members pension until the deceased member reaches the age of 80 years. Statutes for the social security benefits in the Fishermen’s pension and social benefit scheme are similar to those for the social security benefits scheme in the Farmer’s pension and social benefit scheme. Disablement benefits offered under this scheme includes permanent partial disablement and permanent total disablement. Members have two options in obtaining disablement gratuity benefits. Option 1 consists of the payment of the stipulated gratuity benefit plus all payments made by the member to the fund and any interest accrued from these payments, whilst option consisting of not claiming the benefit and obtaining a monthly payment upon reaching the vesting period. Similar, in the death gratuity benefit, the legal heir of the deceased member has the option of claiming the deceased benefit plus all accrued payments and interest made by the deceased member, or the spouse of deceased member is entitled to claim the pension till the deceased contributor completes the age of 80 years. In the event, ‘the pensioner dies while drawing the pension, and the money that he/she had already drawn as pension is less than the equivalent of the total contributions he/she had made and its accrued interest, the spouse or the legal heir of the deceased is entitled to the balance payment in his/her (deceased) account’. Note, the gratuity benefits that members are entitled to under the social security benefits scheme in the Fishermen’s pension and benefit scheme is the same as the gratuity benefit entitlement for disablement and death in the social security scheme of the Farmers’ pension and benefit scheme (Table 4.1) Default rate in the Fishermen’s Pension and Social Security Benefit scheme is two and a half years, or the failure to make ten continuous quarterly payments to the scheme. A standard grace period of 30 days is provided for members to make outstanding payments without any additional charges. Failure to make the outstanding contributions during the grace period results in the charging of interest on the outstanding payments. The interest rate on outstanding contributions is established at the discretion of the AAIB. Current interest rate for outstanding contributions established by the AAIB is 14%. The exit procedure for members in the fishermen’s pension and security benefit scheme is similar to the exit procedure for members in the farmers’ pension and benefit scheme. Fishermen can exit the scheme if they obtain permanent employment in government sector or the private sector in which there are mandatory retirement schemes, as this disqualifies them from participating in this scheme66. Further, members can also exit the scheme if they move to higher income category, or they are migrating67. Members who exit the scheme are entitled to a full refund of all contributions made to the scheme, plus any interest accrued from these contributions.[20]

Legal framework of AAIB

Implementation and managing of both the FSP and FSPS has been assigned to the the AAIB was established in Sri Lanka through the introduction of Agriculture Insurance Law, No. 27 of 197369. Introduction of this law resulted in the Agriculture 66 ibid 67 ibid 68 ibid 69 Agriculture Insurance Law, No. 27 of 197337 Insurance Scheme which was implementing and managing insurance schemes for the agriculture sector under Crop Insurance Act of 196170 been replaced. Introduction of the Farmers’ pension and social benefit scheme in 1987 and the Fishermen’s pension and social benefit scheme in 1991 resulted in the expansion of the activities of the AAIB to include the implementation and management of these two schemes in 1999. As the agent authorized in the management of these two schemes the AAIB has the authority to makes and regulations pertaining to the AAIB board with respect to operating these two schemes, to maintain financial, actuarial and operational reports pertaining to the functions of these two schemes, to monitor the two schemes and make changes in areas where it is authorized to do so, employee managers, employees and other individuals necessary for the effective operation of the two schemes, and to conduct activities which in the opinion of the board are essential to ensure the effective management and operation of these two funds[21]

Weaknesses of existing informal schemes

Findings from the empirical analysis revealed a number of weak points in the current informal retirement benefit schemes ranging from operational issues, to financial issues, the limited ability for the schemes to provide social security, and legal limitations of the schemes. In order to determine the ability of the scheme to provide adequate social security to members, the researcher focused on two key questions i.e. Do these schemes in their current format generate adequate social security for members? and are the current schemes financially self-sufficient. Responses from the participants indicate that current returns from the schemes is essentially worthless for individuals below 50 years of age joining these schemes. Further, most participants indicated that the real value of money of the pension is likely to be significantly eroded over the lifetime of the pensioner. Most respondents stated that the main reason for the ineffectiveness of the pensions schemes in the current systems to provided effective social security for members after retirement is on account of the fact that the pension systems in these two schemes are based on an average life expectancy of 10 years after the reaching the age of retirement, when actual life expectancy values are significantly higher than this assumption. In terms of the sustainability of the two schemes, most respondents stated that two schemes are not financially self-sufficient and will require significant state funding in the future in order to meet pension obligations. Further, according to the respondents the ability of the state to support the financial needs of the two funds is a concern given that it is yet to provide the financial commitment it made towards these two funds at the implementation stage. Legal weak points identified from the empirical research related was the lack of the teeth in the existing schemes to enforce contributions. Respondents stated that unlike formal retirement benefit schemes where legislation makes it mandatory for workers in the formal sector to enroll and make mandatory contributions to formal retirement schemes throughout their working career in the formal sector, retirement benefit schemes are voluntary. This has resulted in enrolment in voluntary schemes been extremely low and been dependent on marketing factors such as the effectiveness in which AAIB employees 40 communicate the need for informal sector to enroll in pension and social benefit schemes, and the extent to which workers in the informal sector perceive the importance of having retirement benefit schemes. Most respondents stated that workers in the informal sector have low interest in joining retirement schemes due to extend family system prevalent in Sri Lanka. Further, respondents stated that the lack of laws to enforce collection of outstanding dues from members was another factor which has contributed to the high default rate in these two systems. Financial weak points of two systems was that average amount paid as pension is extremely low. Findings from the interviews indicate that average monthly pension of these two systems ranges between Rs.1,000 to Rs.5,000 and is insufficient to meet the day-today needs of members post retirement. In addition, some respondents stated that requiring members to make two payments annually in the case of the farmers’ pension and benefit scheme, and four quarterly annual payments in the case of the fishermen’s pension and benefit scheme placed to much of a burden on members, and that this has contributed to the high default rate in the two systems.

Recommendations

Findings from this legal study of retirement benefit schemes for workers in small scale enterprises in Si Lanka indicate that whilst there is comprehensive legislation pertaining to the farmers’ pension and social benefit system, and fishermen’s pension and benefit system which covers the operations of these systems, participation in these systems, and benefits of these systems extensively, the voluntary nature of these systems has resulted in low participation and high default rates. In order to address these weaknesses, the following should be implements;

❖ Introduce legislation which makes workers, owners and lessees working in the farming and fishing communities in Sri Lanka contribution to these schemes compulsory. In order to ensure compliance with legislation issued in this regard, fines and jail terms should be introduced for those failing to participate in these schemes,

❖ Legislation should be introduced which provides AAIB with the power to prosecute members who default continuously for more than two and a half years. In addition to fines and penalty interest, jail sentences should also be introduced for members who deliberately default on making the annual contributions,

❖ Change the current regular payment system to a monthly payment system for both the farmers’ pension and benefit system and the fishermen’s pension and benefit system. This in turn should reduce the current high default rate,

❖ Increase the monthly pension to a level which ensures adequate social security for members post retirement. Given that findings from the study revealed that the current pensions paid out from these systems are essentially worthless for those under 50 years of age, the pension system should be redesigned to ensure a monthly pay-out which guarantees the social security of members post retirement

Conclusion

A key objective of this study was to identify the retirement benefit schemes for workers in small scale enterprises in Sri Lanka. Findings from the doctrinal research and the literature review indicate that Farmer’s Pension and Social Benefit Scheme is a retirement benefit scheme which has been developed exclusively for owners, lessees and workers in the Sri Lankan farming community, whilst Fishermen’s Pension and Social Benefit Scheme is a retirement benefit scheme for owners and workers in the Sri Lankan fishing community. Further, findings reveal that these two schemes are voluntary schemes which require members to make annual contributions. Enrolment in these schemes guarantee members a monthly pension after reaching the vesting age and also provides a number of social security benefits to members and the legal heirs, subject to complying with the stipulated payment conditions. Determining the effectiveness/impact of the current retirement benefit schemes for workers in small scale enterprises was another key objective of this study. Findings from the study reveal that the effectiveness/impact of these schemes is limited with a low number of members and the low growth rate of participants. Findings also revealed that the current pensions received by members these two systems is essentially worthless due to inflation and the high life expectancy of members after retirement. Identification of the weak points of the study was another key objective of this study. Study findings revealed that the two schemes are not financially self-sufficient and will require significant state funding in the future in order to meet pension obligations, that the pay-out in the form of pensions from these schemes is essentially worthless for individuals below 50 years of age joining these schemes, and that the absence of laws making contributions to these funds compulsory has resulted in low participation rates and high default rates.

[1] G Tilekaratne and S Jayawardena, ‘Social Protection in Sri Lanka: Current Status and Effect on Labour Market Outcomes’, 2015 accessed

[2] G Tilekaratne and S Jayawardena, ‘Social Protection in Sri Lanka: Current Status and Effect on Labour Market Outcomes’, 2015 accessed

[4] HelpAge, ‘Why social pensions are needed now’, 2006 accessed

[5] A Abayasakera, ‘Pension coverage in Sri Lanka’, 2019 accessed

[6] Perera (1989), Emerging issues of population ageing in Sri Lanka, Bangkok: Economic and Social Commission for the Asia Pacific (ESCAP)

[7] Farmers’ Pension and Social Security Benefit Scheme Act No.12 of 1987

[9] Farmers’ Pension and Social Security Benefit Scheme Act (Gazette No.452/12 of May 7, 1987

[10] Farmers’ Pension and Social Security Benefit Scheme Act (Gazette No.522/6 of September 7, 1988)

[12] Farmers’ Pension and Social Security Benefit Scheme Act (Gazette No.452/12 of May 7, 1987)

[13] Farmers’ Pension and Social Security Benefit Scheme Act (Gazette No.452/12 of May 7, 1987)

[14] Agriculture and Agrarian Insurance Act, No.20 of 1999

[16] Fishermen’s Pension and Social Security Benefit Act (Gazette of 1996.09.09)

[17] Fishermen’s Pension and Social Security Benefit Act, No. 23 of 1990

[21] Section 11 of the Farmers’ Pension and Social Security Benefit Act No.12 of 1987, and in Section 13 of the Fishermen’s Pension and Social Security Benefit Act No. 23

*Authors are third Year LLB (Bachelor of Law) Undergraduates at General Sir John Kotelawala Defense University