By Kumar David –

Prof. Kumar David

Global capitalism still wobbling seven years after recession began

The IMF hedged its bets but concluded cautiously on an optimistic note in its 27 April World Economic Outlook document and press briefing. Jan Hatzius, Chief economist at Global Investment Research at Goldman Sachs, says “There is more light than shadow, but it’s a relatively finely balanced picture”. The Economist in its June 13-19 issue on whether there is a US and global recovery comes down gingerly on the positive side. They highlight different spanners in the works; the IMF the hangover of debt (“legacy problems”), Hatzius that when the Fed raises interest rates, possibly in September, it will have disruptive global effects, and the Economist that central banks and policy makers have depleted their arsenal of recession fighting tools and will be empty handed if recession returns. I will summarise this variegated picture without reference to last weeks 61.3% vote in Greece against austerity and neoliberal economics, an expression of confidence in Tsipraz-Syriza and shockwaves for Euro, European finance capital and possible Grexit. These topics deserve full length treatment on their own.

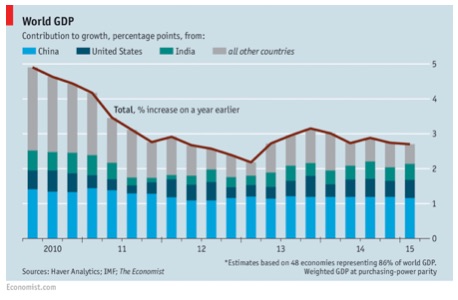

First, a startling reality can be explained using a graphic tucked away on the last page of the same issue of the Economist. In the diagram, look at the share of different actors in global GDP growth and focus on the four most recent quarters. Global GDP grew at about 2.7% (annualised rate), but of this 1.2% came from China while the USA and India contributed about 0.5% each. All the rest of the world, the EU, Japan, Africa, Middle East, Australia, Russia and all South and Central America contributed a mere 0.5% to 0.6% to global growth; a huge drop from over 2% (about half) just five years ago. I am nonplussed that in their obsession with a possible US recovery, this sustained petering out of the collective output of all countries other than China, USA and India has received little press from pundits.

Secondly, the US economy has been a yoyo; ok, omit the first three years after 2008 – the downfall of US banking – and look at behaviour from about mid-2011 on the chart. The US has blown hot and cold from quarter to quarter. The most recent data for April and May 2015 (second quarter, not on chart) indicates negative investment and export growth but June shows robust improvement in job creation; an irregular stagger. But then, unemployment has dipped below 6% and job creation has been strong, giving forecasters’ confidence that the US recovery though modest (below 3%) is here to stay.

Secondly, the US economy has been a yoyo; ok, omit the first three years after 2008 – the downfall of US banking – and look at behaviour from about mid-2011 on the chart. The US has blown hot and cold from quarter to quarter. The most recent data for April and May 2015 (second quarter, not on chart) indicates negative investment and export growth but June shows robust improvement in job creation; an irregular stagger. But then, unemployment has dipped below 6% and job creation has been strong, giving forecasters’ confidence that the US recovery though modest (below 3%) is here to stay.

The steady decline in China’s contribution to global growth from 2010 to 2015 was expected as Chinese GDP growth fell from over 8% to possibly as low as 6% (The bloodletting on the Shanghai stock market last week wiping out $3 trillion was not expected!) The slowing down of growth is good for the Chinese people as it is time to turn off the gush of breakneck expansion that fattens the wallets of greedy businessmen and channel resources into socially necessary healthcare, education, low income housing and the hinterland. In India, robust growth took root in mid-2013 and the Modi administration can sustain 7% growth for the remainder of its term. What a wonderfully lop-sided world! Does the data not beckon trouble down the line in “all other countries”?

The curious mountain of debt

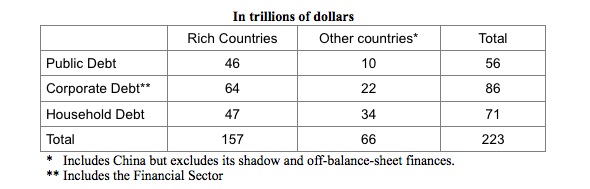

Economists at ING, a Dutch multinational bank and financial services corporation, report that the world is drowning in a tsunami of $ 223 trillion debt distributed in public (government), corporate (company) and household (mainly mortgages) sectors. I have reprocessed the ING findings into a table.

At first sight these numbers are so large that they are unbelievable – for comparison, global GDP is $70 to $75 trillion and US GDP is $17 trillion; the total GDP of the rich countries is about $42 trillion and total for other countries including China is about $30 trillion. If there is $223 trillion in global debt, well there must be creditors worth $223 – who are they! Everyone can’t be a debtor; someone must be a creditor and a flush one at that. What the economists don’t tell you are a few things that many of them don’t grasp anyway. If A owes B $100, B owes C $100, C owes D $100 and D owes A $100, in the eyes of these profoundly clever folk, the circuit is awash with $400 of debt. My grandmother will scoff: “Balderdash there is no debt at all!” So circularity accounts for part of the jumbo numbers. True, interest rates round the circuit will differ and some in the loop may be more dicey (risk prone) than others so that if the loop fractures at one point all may drown.

At first sight these numbers are so large that they are unbelievable – for comparison, global GDP is $70 to $75 trillion and US GDP is $17 trillion; the total GDP of the rich countries is about $42 trillion and total for other countries including China is about $30 trillion. If there is $223 trillion in global debt, well there must be creditors worth $223 – who are they! Everyone can’t be a debtor; someone must be a creditor and a flush one at that. What the economists don’t tell you are a few things that many of them don’t grasp anyway. If A owes B $100, B owes C $100, C owes D $100 and D owes A $100, in the eyes of these profoundly clever folk, the circuit is awash with $400 of debt. My grandmother will scoff: “Balderdash there is no debt at all!” So circularity accounts for part of the jumbo numbers. True, interest rates round the circuit will differ and some in the loop may be more dicey (risk prone) than others so that if the loop fractures at one point all may drown.

Some debt will never be repaid. If a central bank prints billions to buy treasury bonds which the treasury never redeems (more precisely, keeps recycling) it is simply printing money to keep Zimbabwe’s Mugabe, Venezuela’s Maduro, or for that matter the US Federal Government afloat. In the long run some of it will be inflated away; a billion lent on treasury bonds 50 years ago will fetch less than 10 million in surrender value in real terms today, leaving aside interest related accruals. Nevertheless, though all banks create fiat money when the bulge is this big it is not make-believe, it will not all evaporate away.

The third point is that a large part of government borrowing is from pension funds and social security treasure chests which are continuously replenished; a letter of demand on doomsday never arrives as one loan is repaid and a larger one simultaneously taken. More secretive is finance capital’s use of derivatives (complex financial instruments and hedges) to, quite frankly, bamboozle the public. Nick Dunbar said more than 10 years ago in Risk magazine (June 2003); ‘It is now widely known that since 1996, Italy’s Treasury has regularly used swap transactions to optically (sic!) reduce its publicly reported debt and deficit ratios. Such trades are controversial, and subject of fierce debate”. In Risk January 2002 Italian academic Gustavo Piga accused the Eurozone of “window dressing” public accounts using derivatives. The worst such manipulation is Goldman Sachs ‘Mega-Deal for Greece’ where, in cahoots with a previous Greek government, a complex web of currency deals and swaps were used to cook the books. Mind you nothing was justiciably illegal as with all finance capital’s mega scams; banks and money barons look after themselves leaving pensioners and wage earners to rot.

After making allowance for circularity of debt, and never-repay central bank holdings (which relate to public debt only) and for subterfuge, there still remain tens of trillions of credit that someone must own. Who? The “owners” of this massive loot are the world’s financial moguls, billionaire investors and the stinking rich. The 1% own it; investment houses trusts and banks only collect and organise the finances of corporations and individuals. Hence part of the global debt crisis is nothing other than another face of the massive inequality of global wealth in late capitalism. If the 1% hold 90% (or whatever) of global wealth, there is your answer to the ‘who owns it’ question. According to the Boston Consulting Group global private wealth stood at $165 trillion in 2015, which fits my analysis. At root, the standoff between creditor and debtor is also a class conflict; German finance capitalist versus Greek citizen.

The IMF’s expectation in its World Economic Outlook presentation is for somewhat higher global growth (3.5%) than the authors of the chart that I have shown (Haver Analytics, IMF, Economist) anticipate. This is to do with the way different country contributions are weighted, but there is no dispute that aside from China, the US and India the outlook for the rest of the world is bleak. ING’s fears that the huge private and public debt overhang is a roadblock that cannot be cleared is corroborated by the IMF. My friend and one time colleague Professor Harsha Sirisena in New Zealand impishly calls for mega global debt forgiveness: “There is no other way, just write most of it off”; he is probably right.

A depleted arsenal

Theoretically, there are two conflicting ways for capitalism to climb out of a recession – in practice a mix is used – the Austrian or now mostly out of fashion (except for torturing Greece, but that’s for a different purpose; to force regime change) neoliberal approach, or the bastard-Keynesian way. The former entails budget cuts, savage austerity and welfare, pension and wage cuts, till the economy is “cleansed” and growth commences. The alternative, the classical Keynesian trajectory was government spending on infrastructure and employment creation as in the New Deal of the 1930s. Today this classical approach is drowned out by pumping money (Quantitative Easing or QE) into the treasury and banks, tax cuts for the rich and low interest rates. To rescue finance capital from near death, it is not employment generation through public spending but money in the pockets of big capital that is expected to revive the economy”. This bastard-Keynesianism is not to be confused with Keynes’ prescriptions.

Interest rates are nearly zero (or in the case of Japan, real interest rates are negative) and hundreds of billions are being pumped into treasury and bank bonds by central banks. If recession bites again there is no more space to lower interest rates, shave budgets or pour more money via QE; the Feds balance sheet now stands at $44 trillion. Inflation, asset price bubbles and crazy stock market gyrations will aggravate future crisis. This scenario keeps the editors of the Economist awake at night; sans interest rate tools, fearing that more austerity will provoke unrest (hence the conspiracy for regime change in Greece) and having reached the limit of rolling the currency press, if recession strikes again soon central banks and policy makers in the great capitals stand defenceless.

The high US dollar and low commodity prices indices are a complication that is good for some and problematic for others. The high dollar is good for US trading partners but it is pushing the American trade balance deeper into the red – the US net trade balance worsened at an annualised rate of 7.5% in the first quarter of 2015. The relative decline in the value of the Euro and the Yen is of course raising hopes in these two regions of better export performance but their own data, paradoxically, does not support the expectations. The global economy is awash not only with debt but also contradictions.

There is another complication that I have space only to mention; commodity prices. The price of oil is down 43% compared to $110 a barrel 12 months ago; global food prices down 18% and industrial goods down 12%. Despite near zero interest rates for years and the gush of the currency press, inflation, paradoxically, is keeping its head low. This is good for consumers, bad for producers and manufacturers; good for some countries and bad for others. I will take this up at greater length some other time.

EW Golding / July 12, 2015

Comment made on Sunday 12 July.

At this moment the greatest source of instability is the fate of the Euro in the next few weeks. Today (12) EU leaders and European finance capital will decide whether to kick Greece out of the Eurozone. If they do so the medium term consequences are hard to predict. The author should discuss the Greek-Euro crisis in depth.

/

Bruno Umbato / July 12, 2015

Thanks for your insights into the world economy …

But, why u suddenly stop writing about your success in ‘regime change’ project and the way you guys deceived the public by putting ‘yahapalana’ facade?

Could u remember that you even lift the profile of Champaka R after his book ‘Power and Power’ launch when he was in the other camp?

Just tell the public whether you and Champaka were working together in the ‘regime change’ project ..

It is very interesting hear the truth behind from you, Kumar …

/

vas / July 12, 2015

The writer forgot to mention Iceland who were in a similar predicament as Greece. They are recovering well after the banking collapse of around 2010. They got out of the mess by going bankrupt and relegating on the debt, ignoring the IMF/WB advice, incarcerating the Bankers and the politicians who were corrupt and establishing a new economic frame work for the benefit of the Icelanders.

SL today is virtually bankrupt.but our politicians are vying for their personal gain. No one has until now come up with the answers to our predicament , which is bankruptcy. It is time the country wakes up from its slumber to answer this very important the predicament of the country. Should we not do what the Icelanders did incarcerate the corrupt Bankers and Politicians.

/

Pacs / July 12, 2015

SL is worse than Greece. They demand everything without working.

/

whywhy / July 12, 2015

More than 90% literate (supposedly educated) and

praised by all hues of politics as intelligent,

always expect for more and vote only for more.

Natural that everyone will want more but is it

logical to offer more to an unaffordable level ?

Who got the backbone to tell the truth that we

can not afford the luxuries of developed world

which work hard to sustain the developments and

wealth they earned for centuries ?No government

is making an honest approach to collect direct

taxes to develop the country with the participation

of the citizenry. Public involvement in the govt

functioning is not encouraged and only used as

beggars from the govt by all political parties.

Goodies galore at election times and after that ?

Pay back time ? Educate the people about where

the world going and get their support to manage

our whatever existing condition so that we keep

in shape before becoming another Greece !

/