By Kumar David –

Prof. Kumar David

Neoclassical burnishing makes a fictionalised version of actual capitalism: Minimal utility of neoclassical economics!

The critique of neoclassical economics that we are familiar with is political and ideological. The villains are strike breaking, union bashing Regan-Thatcher, bigots like Freidrich Hayek who mentored Chile’s military dictator Augusto Pinochet and a privatisation obsessed IMF of structural adjustment infamy. This critique of neoliberalism, which is neoclassical economics spiced with a right-wing political programme, is a passionate rejection of this political ideology.

The book that is up for review today is different, it’s not political, it’s written for economics scholars and explores the fundamental categories on which neoclassical economics is built, that is; ‘rational’ consumers, U-shaped supply curves, flat demand functions and the fiction of an equilibrium at which marginal-utility equals marginal-cost. The author’s scalpel eviscerates every one of these categories from the inside that is from within economic discourse and using empirical economic data. This book will resonate for a long time.

Capitalism: Competition, Conflict, Crisis; by Anwar Shaikh, Oxford University Press (2016), pp 979, $50 hardcover, makes heavy reading. The prose is turgid, references to published literature profuse, and the inclusion of mathematical sections in text and appendices require familiarity with algebra, a smattering of calculus and a little bit of regression theory. Another matter that makes the going hard, but constitutes the book’s great strength, is the wealth of empirical data that grounds analysis in actually existing capitalism, current and past. In this Shaik reverts to the materialist and empirically grounded approach of the great classical economists; unlike latter day neoclassicals who snatched ideologically loaded delusions out of the theoretical aether.

Shaik, of Pakistani origin, started as a Princeton educated physicist, but mutated to Professor of Economics in the New School in New York. This magnum opus he says has been in preparation for 15 years and I can discern the inputs of graduate students in working through spread-sheets, graphs and computational algorithms. There is no way I can do justice to a 1000 page tome that’s heavy to even carry around in a 2500 word review. In any case if I get stuck into detail and derivation I will lose all but the nerdiest of readers. My objective is to explore interesting and controversial arguments but at the same time to try to hold the attention of all who have some grounding in the dismal sciences. I have chosen just three aspects to follow through; Shaik’s demolition of neoclassical economics, his theses on real competition and third his summary of Kondratieff long waves.

Decapitation of neoclassical economics

Classical economics refers to the work of Smith, Ricardo, Malthus, Marx and John Stuart Mill but originated with Sir James Steuart who in Principles of Political Economy (1767) preceded Smith’s Wealth of Nations (1776) by nearly a decade. Neoclassical economics (NCE) got started in the 1870s with William Stanley Jevons in England, Carl Menger and the Austrian School which was sceptical of perfect market theories, and Leon Walrus (perfect competition and general equilibrium) in France-Switzerland, and led on to von Mises and Hayek in the Twentieth Century. Till recently, perhaps even now in backward university departments, neoclassical theory is taught to unsuspecting undergraduates as “mainstream” economics.

The core concepts of NCE are: a) a utility maximising ‘rational’ consumer, b) production functions whose marginal costs steadily rise with output, c) firms as price takers facing flat demand functions, d) the macro (whole economy) as a scaled up version of the micro (the firm) and finally the great fiction e) a smooth and stable equilibrium state in which marginal-utility equals marginal-cost in macro discourse. Shaik puts every one of these concepts to the test, not by counter posing alternative ideological categories but from empirical data – national statistics (USA and Europe), evidence from business journals and company sources, and data driven studies by dozens of research units and business schools. The reference list runs to 37 pages of small print.

The social moron

For the reasons I indicated and to keep the length of this review manageable I will present the critique of (a), (b) and (e) only today. The standard bearer of NCE, its uniform stereotype, its homo economicus, is the ‘rational consumer’. Invariant in habit, unleavened by class, social environment or circumstance, the social moron, a utility maximising automaton is unknown in real life,but the mores of this mythical being is what the NCE universe hinges on. All two-penny economists swear to the existence of this yeti. The wealth of data accumulated by Shaik says that businessmen, company executives and real world capitalists have no use for this fairy-tale. Quite to the contrary, companies research their consumers to distraction; Goole and Facebook data-mine the smallest nuance of variation; sellers investigate differential features to tinge product variation and target advertisements. The social moron of homogeneous habit, the NCE archetype, is an unknown creature in the world of actually existing business.

It gets more interesting. Shaik and his students modelled four types of consumers and also made samples that mixed some of each type into an aggregate brew. The four types are the NCE social moron, a more heterogeneous moron with varied utility functions, the Whimsical Agent whose choices incorporate impulsive behaviour and fourthly the Innovative Agent who improves choice step by step learning from outcomes and other agents. Budget constraints, income distribution, price elasticity and necessary goods versus luxury goods distinction, were inserted into the programs. Guess what! In the aggregate, by tweaking model parameters, different agent types or combination of types, could all be made to produce any desired aggregate (macro) consumer-function shape. That is to say the aggregate is robust to type assumptions.

What is the significance? It is unnecessary to invent a patently false agent. The project that NCE sets out to accomplish is an ideological not an economic one. Have you ever met a donkey of a real businessman who sets his production targets, prices and mark-ups using consumer marginal utility derivations and potential equilibria in perfect markets? NCE’s objective is to lull the unwary into illusions of supra class rationality of its model. It is a pseudo-science that gilds capitalism as socially optimal and economically efficient.

Imagined production functions

NCE’s invariable production function (cost against increasing output) is steadily upward pointing; the more you produce the more it costs; that’s fair enough though adjustments have to be made for start-up and fixed costs. However NCE’s crucial feature is that marginal-cost (the cost of making one more unit) must steadily increase. (The 100-th unit must cost a bit more than the 99-th unit). This is what supplies NCE with smooth upward sloping marginal-cost curves without which its perfect-market equilibrium theory evaporates.

Shaik has a 55 page chapter of data obtained from business economists, process observations and industry studies to show that this is bollocks – it is more honoured in the breech than observance. Shift work, organisational and technical factors, physical stock-flows, inventories, and capacity reserves for unforeseen needs, invalidate NCE’s cost curve exemplar. The latter is a far cry from what happens in the real world of industry and production. Real world marginal cost versus output graphs may be upward or downward pointing, jagged or irregular and spikey or kinky. Shaik quotes a survey that found that 94% of business leaders chose a downward, not upward sloping marginal-cost plot as typical, contradicting the representative shape on which NCE equilibrium mythology hinges. Real business marginal-cost curves point in other directions than NCE’s holy-cow archetype.

The cul-de-sac of an equilibrium state

Shaik reserves his sharpest dagger for the evisceration of NCE’s central concept, the market clearing equilibrium state in which declining marginal utility intersects rising marginal cost. In this Benthamist utopia, utility and profit are jointly optimised, peace, profit and property prevail and capitalism is the best of all possible worlds! I have discussed the flawed functions assumed in NCE,s utopian shapes, alien to classical economics and strangers to company board rooms and production managers. But this is not Shaik’s central critique; the crux is that real world is not a streamlined process gliding to equilibrium. Perfect competition theory and its anodyne equilibrium states are fiction. To see capitalism at work turn to real competition in prevailing markets; there you will see a very different, a very turbulent process.

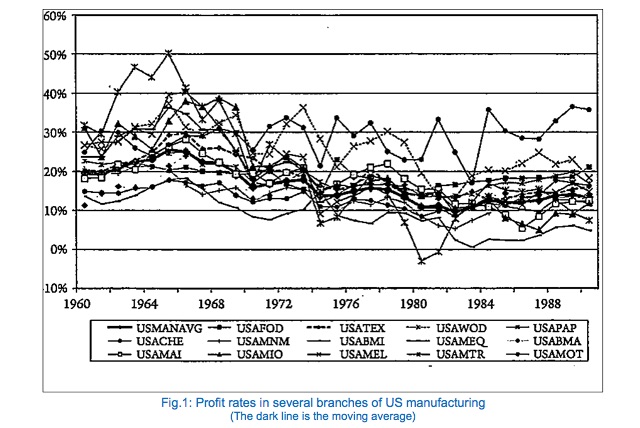

Fig.1 (Shaik’s figure 7.14) shows the movement over time of the rate of profit in a range of US manufacturing sectors. Accept profit fluctuation as proxy for price fluctuation. Then when the price indices of a variety of suppliers grouped by branches of industry (cars, carpets, canned beer etc.) are plotted over time, we see turbulent flow, the feral reality of fig.1, which rebuts the imagined nirvana of harmonious equilibrium prices.

Firms unavoidably overshoot and undershoot the optimum (unknown in advance). Producers price too high or too low; new technology introduced by competitors creates panic; market share is won and lost. This real world is a turbulent process of competition gravitating to an industry-wide average profit rate which itself proves as mercurial as capitalism itself. Imagine the turbulent rush of a river over rapids and rocks, as water flows it rushes and gushes, momentary torrents are thrown up and down; gravity and hydrology impose turbulent order within this disorder. Such is the competitive process of real capitalism. Such is empirical, observed data that classical economists Smith, Ricardo and Marx used as raw material. The schoolmen of NCE ilk are different says Shaik.

Real world competition

What I have said so far is a brief outline of Part I, a 250 page Foundations of Analysis section. Part II is 300 pages on Competition with chapters on Basic Theory, Perfect & Imperfect Competition, Competition & Prices, Finance & Interest Rates and the chapter concluding the section is Exchange Rates. My job is not to try to summarise all this but to give you a two paragraph glimpse. Shaik’s leitmotif is that two overriding imperatives establish the nature of capitalism; compulsion to profit and ubiquitous competition. The dynamic, turbulent overlap and conflict between these two imperatives, has and will always determine capitalism’s historical path.

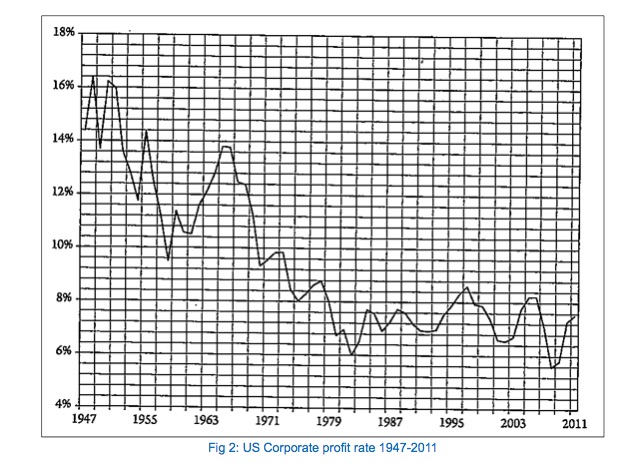

Fig. 2 (Shaik’s figure 2.11) shows the fluctuations of the business cycle of about 8 to 10 years riding on the long term secular decline of the US corporate profit rate from the end of the war to 1980. Suddenly after 1980 only the business cycle remains and the secular trend disappears due to Regan’s assault on worker’s wages and union activity, that is to say state interference suspended the market and capitalism’s natural processes. NCE theory cannot explain any of these real world events, neither the persistence of business cycles nor the tendency of the rate of profit to fall. One has to turn to empirical studies of real world competition for that. And perish the thought of any tendency of the rate of profit to fall! Wasn’t this what that horrible man Marx was talking about?

Kondratieff long waves

Part III is devoted to the turbulent dynamics of capitalism and the chapter headings are Rise & Fall of Neoclassical Macroeconomics, Classical Macro-dynamics, Wages & Employment, Money & Inflation, and Recurrent Crisis. In the first of these chapters Shaik continues his critique of NCE at the macro level and takes aim at its progenitor mathematical Leon Walrus. The achievements of Keynes initially with a mathematics degree, and Kalecki an engineering degree, are acknowledged but their imperfect completion models are modifications within the perfect competition paradigm and therefore its paradigmatic prisoner. In the next chapter Shaik explores the macro-dynamics of the classical economists, grounded in real (opposed to “perfect”) competition. The chapters on wages, employment, money and inflation, inter alia take a negative stance Milton Friedman’s ideology. All the presentations are detailed and heavy with graphs, tables, empirical data and a little mathematics. I will have to leave it to the specialist reader to get hold of a copy of the book (a steal at $50 on Amazon) and work away at it.

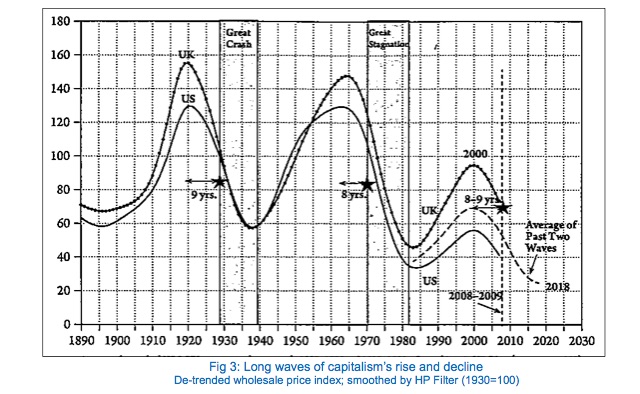

I now pick up from the final chapter the discussion of a fascinating twist, long waves. Nicolai Kondratieff a proponent of Lenin’s New Economic Policy (b. 1892 – arrested on trumped up charges in 1930 and executed in 1937) authored a famous set of charts while in prison, depicting long 40-50 year waves in the rise and decline of the capitalist economy. Shaik has updated the charts to 2011 and improved the presentation. The data is “de-trended” (presumably continuously inflation corrected) and passed through an HP filter to remove confusing wrinkles and rumples. The data here is for the wholesale price index, but employment or profits could have been used instead. Kondratieff and Shaik following him prefer wholesale price.

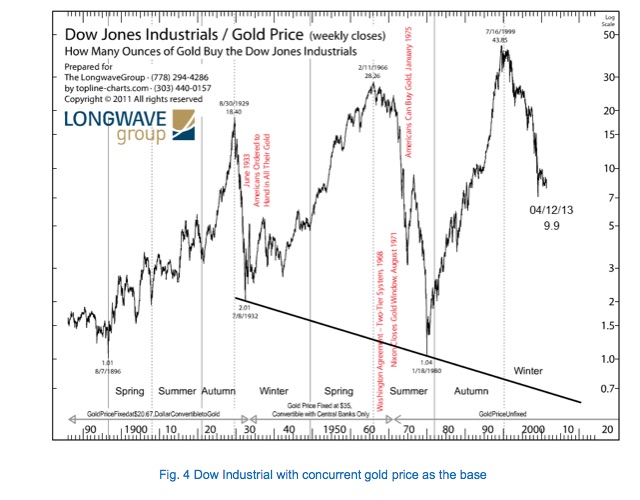

Fig. 3 (Shaik’s, figure 17.1) shows three clear waves, and if we go from trough to trough they are 1897-1939, 1940-1982 and the last one from 1983, transiting the 2008-2009 crisis and according to Shaik’s processing to bottom out in 2018. Three waves, 1790-1849, 1850-1896, and one starting in 1897 and nearing its trough at the time of his death in 1937 were examined by Kondratieff. Recent waves seem to be 40 to 45 yearsduration but older waves were a little longer. Long waves are not to be confused with the better known 8 to 10 year business cycles clearly visible in fig. 2. Web searches throw up interesting diagrams such as fig.4 which is the Dow divided by the concurrent gold pric. The same two and a half waves as in fig. 3 are clearly discernible.

The mechanism underlying the business cycle is understood by conventional and classical economics and the tendency of the rate of profit to fall conforms to Marx’s eponymous thesis in chapters 13-15 of Kapital III. But in my view no rigorous theoretical reasoning has been adduced to explain Kondratieff long waves. Marx’s qualitative prophecy of periodic catastrophic crisis, strewn across his opus is the closest we get, but this is generic homily not rigorous analysis. This conundrum is a good point at which to close my review.

A sour note

I am duty bound, more for the sake of a prospective second edition than as a warning to the reader, to point out that there are rather too many editorial slip-ups. There are references to the wrong figure number in the text, an incorrectly calculated column in a table, reference to a non-existent appendix, incorrect dating of a Marx text, and symbols sometimes not defined or badly chosen (surprising for a trained physicist) and there are one or two slips in the maths. Allowing for size, complexity and scope of text this is understandable and does not detract from the reading. A paperback second edition is a chance to straighten all this out and reach impecunious readers and third world graduate students.

New Vanguard / June 20, 2016

Professor. Kumar David

Thank you for such an informative article. The boom-bust cycle is a real eye opener 2020 does not look very promising. Thank you also for the refernce to hard evidence which is so much lacking in many economic analyses.

It should have been long known that perfect competition does not exist, simply look at the different prices of the same product. What has happenned is that the world has become a lot more turbulent.

/