By Kumar David –

Prof. Kumar David

Part III: Peering into a technically rational crystal ball

This concluding third part of the series outlines a conceptual proposal for the reorganisation of the electricity supply industry (ESI) in Lanka; it is conceptual, not a blueprint cast in stone. The motive is to embrace new technologies and business practices and to meet emerging challenges. Privatisation is inimical when national or regional monopoly settings (‘public goods’) prevail – transmission ownership, operation and system control is an example; similar functions in distribution is another example. Only a lunatic will contemplate two overlapping transmission systems in one country or imagine two distribution networks under roads and over farms and homes in a locality.

Where competition is desirable is in electricity generation. An IPP (Independent Power producer) may be domestic, foreign (FDI) or joint-venture capital. There was a global trend towards a power market in the 1990s but after the catastrophic California Power Market crash in 2001 the trend receded. Globally, recent acquisitions signal a turn to consolidation, but irrespective of market type, the ESI is responding to advances in technology and new options in energy supply. Global fashions however must be modified to a local context; otherwise one will be shooting at abstract targets.

Smaller gas-fired plants are cost competitive in capital and operation in countries with gas deposits. This makes distributed generation attractive. But in Lanka this is predicated on a gas distribution network for industry and transport in general; otherwise better stay with centralised power stations and ship out electricity. In a trade-off between transmission losses and capital investment in special purpose pipelines to ship gas to power stations only, the former wins.

Mini and micro generation (less than 10MW; hydro, wind, rooftop PV and wood based) and industry based standby plant is on the increase, but electricity sector reorganisation is not warranted to deal with these pimples. Rooftop solar (as distinct from large utility size solar farms) even if it adds hundreds of MW of simultaneous injection at high-noon on a bright day, can, technically, be handled on-the-hop by distribution entities.

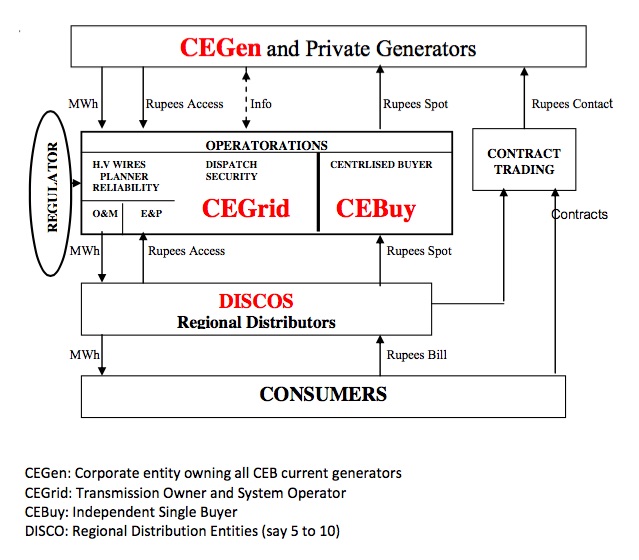

Independence of the system operator-cum-transmission-owner, and independence of a centralised electricity buyer from individual generating companies (including the CEB’s generation arm) is imperative if competition in power supply and the incorporation of large solar (and wind) farms is to be accomplished. Sounds complicated? Hang on; it will be clearer when a typical structure is laid out, so let me take the plunge and sketch a long-term structure; it is premature to discuss implementation stages. The diagram shows functions that currently belong to the CEB split into three blocks – CEGen, CEGrid & CEBuy and Discos. Separate from this is Other Generators, Consumers, the Regulator (a replacement PUCL) and Contracts. Let me lay out the thinking behind this.

The independent grid operator

The transmission system – and its control, management and expansion – is queen of electricity supply. CEGrid must be impartial to all competing suppliers in the market, including CEB generation (CEGen); it must be even-handed to all buyers (Discos). Above all as a national monopoly – provider of a public good – it must be a publicly accountable body like the Central Bank. Think of CEGrid as a court of law adjudicating between plaintiffs (generators) and defendants (distributors).

To achieve these ends it must be independent of all generators and distributors and tracked by a sensible rule-making Regulator. (Currently PUCL and CEB are involved in a procession of petty squabbles; “We told you to do a 20 year plan, how dare you do a 24year plan!”). CEGrid will impose a use-of-system fee on generators and end-users to recoup transmission losses and organisation costs and to procure funds for grid expansion. The principal structural change that I am emphasising today, an independent transmission entirt (CEGrid), is already well established in quite a few countries.

CEGrid can contemplate many innovations. One overhyped novelty is the so-called smart-grid. This is the use of computer intelligence, power-electronic switches, algorithms and the Internet to re-switch lines and devices called SVCs and capacitors so as to enhance operational capability. At least that’s the hype, but I am not convinced that the smart-grid is a game changer or has achieved much in transmission networks. (Distribution is another story; automation and smart techniques have improved reliability between the consumer and the local supply point in many countries). Of course many things can be done without restructuring, but the point is not in the detail; it is that the grid must be free to improve, innovate, keep abreast of developments and not be tied to the apron strings of any power generation company or corporation. For example there has been talk of an up to date system control centre for years, but little has happened. An independent CEGrid will be more motivated and have its own budget; “unbundling” or separation is a concept that deserves scrutiny by stakeholders.

Competition in generation

The big story globally in the 1990s was competition in generation to bring down prices and enhance efficiency. To prepare the ground locally, the generation arm of the CEB will have to be spun off into a separate state-owned entity, CEGen. Or maybe two; a hydro part and a thermal generator like India’s state owned National Thermal Power Corporation, India’s largest power producer. The hydro sector in Lanka has a unique feature; fuel cost is zero but dispatch (water discharge schedules) must respect downstream irrigation and human needs. This imposes constraints on ‘dispatch’ – ‘dispatch’ means running generators and injecting power into the grid.

Reliance, Tata and other mega-players have entered the Indian power market and compete for market share. It is similar in other big countries. But if a truly competitive market is opened in Lanka will there be IPP takers? I am not sure whether IPPs in Lanka only want protected sinecures. Note that competition is not to be confused with the money for jam game that IPPs have been played in this country for 20 years. Fat profits, recovery of investment and guaranteed sales is not risk taking competition. Nevertheless let’s put my doubts to one side and assume that the private sector will respond to a power market, investing in the sector and competing genuinely on the basis of price.

Where will future gas-fired power stations fed from an LNG harbour terminal fit in? I guess construction of the $500 million LNG terminal will be venture between a port authority and foreign capital. Long term ownership will presumably be vested in some state entity because not only power generators but transport and industry will need to access it. We can then conjecture that from say 2025 power growth will average about a 300MW year. The technologies of choice will be gas, clean coal if its reputation is restored, and renewables. Let us conjecture that some of this is undertaken by CEGen but that private developers too will respond. This then is the case for a competitive power market.

CEGen, even stripped of the hydro component will be a pretty profitable enterprise; it could be profitable right now if shorn of the burden of providing subsidised electricity to indigent sections of the population and religious joints. In a competitive power market, subsidies are a societal choice to be met by government, not burdened on a generator. CEGen will be able to drive competitors out of the market since the biggest component of cost, pass-through fuel cost (gas price), will be the same for all. But CEGen has a head start with Norochcholi, whose coal based prices, gas-fired plants will not be able to match – see tables in last week’s Part II.

CEBuy

CEBuy is mostly bits-and-bytes; in manpower and capital it will be a small unit whose job is to clear the market. That is, it will, with the assistance of the Discos, past data and its own expertise, forecast day-ahead demand in say half-hourly time steps for the next day. It will also receive on-line, offers of how much power and at what prices, competing generators are offering. It then clears the market; that is it accepts the cheapest offers for each time step, notifies these generators and informs CEGrid what to expect. Tough luck for generators who quote high though most may be able to sell something at peak time. Buy and Grid must coordinate intimately since dispatch schedules submitted by Buy may be operationally infeasible, making regular iteration necessary.

Real-time demand and day-ahead dispatch schedules will not match exactly, or there will be unexpected events. CEGrid will therefore have ‘balancing power’ agreements with some generators to buy or shed extra power at a moment’s notice. CEGrid may even own some fast acting generators. In my view a better option is to vest control of the hydro complexes (Mahaveli, Kelani, Walawe etc.) in CEGrid. These zero-cost units are not relevant to competition, water storage is vital to both long term irrigation and power dispatch planning, and daily/weekly running of hydro is constrained by downstream needs. The logical place for all this is an energy management sub-unit of CEGrid.

Solar power has a random quality that requires intimate operational alignment with CEGrid. One rationale for disentangling CEGrid into a separate entity is to deal with solar power’s headaches (stochastic, non-dispatchable and without inertia – see Part I). If renewables are going to come in big time, then an independent system control and dispatch entity is useful. You will observe that my case for restructuring is not much based on competition in generation but much more to do with technical rationalities that can be incorporated if CEGrid is independent from CEGen. A further motive for restructuring is that there may be a good case for introducing Discos – next section.

If the power market does not take off Buy can be dismantled and absorbed into Grid leaving a simple three tier structure of a statutorily independent grid which also looks after hydro, a state owned thermal power generator and several regional distributors. It is absolutely essential that the structure, at least at the early stages, be kept simple. Complication will lead to chaos!

I crave your indulgence to address a few words of technical gibberish to engineer readers. I believe fixed frequency AC will remain the foundation of electricity supply for the remainder of this century. Nicola Tesla’s marvellous transformer cannot be supplanted. Then, massive rotating masses will remain the bedrock of frequency and stability management. Photovoltaics and technologies which generate DC and inject power through inverters (power electronic devices) will play a supplementary role, but the AC grid will reign supreme. This essay on ESI restructuring adopts this as a premise.

Discos

Currently CEB distribution is managed by nationwide regional distribution divisions and one semi-independent company LECO. At some point in time maybe we should spin-off this family into many LECO-like independent entities. Since electricity distribution is a regional monopoly (a public good) these entities will have to be regulated and accountable to the public. Since LECO seems to be a success there may be economies and efficiencies of dis-scale in unbundling. On the other hand economies of scale may be lost. Prima face assumptions may prove wrong; why not start with one or two more distant trials (Jaffna Peninsula, Upcountry, Matara and beyond) and see what experience teaches.

I cannot discuss the Regulator (PUSL has to be reformatted if the electricity supply industry is restructured) or explain the box called Contracts on the right because this piece will become longer; I have overrun my usual word limit already. In closing I repeat, my prescriptions are flexible; they are an invitation to further discussion.

*The author’s IEEE Fellowship was for work on ESI Restructuring

Truth / October 2, 2016

Thanks for your articles on power generation. It is good to hear that you are no longer promoting coal power plants.

There is an urgent need to expedite the Wind Power Plant in Mannar or in its vicinity, to avoid the predicted power crisis. The next priority is for the Prime Minister to approve the Chinese investment in Hambantota, together with a Natural Gas power plant to meet the variations in power inputs from renewable energy sources and to meet the peak power demand. It will increase the attractiveness of tapping the natural gas deposits that were discovered within our territorial waters, before they are emptied from the Indian territorial waters in the vicinity.

A free market for power is the way ahead.

/