By Dhanusha Pathirana –

Dhanusha Pathirana

The 2014 fiscal proposals place significant emphasis on fiscal consolidation mainly by tightening tax policy measures while continuing the pattern of relatively high growth of state expenses witnessed in the past eight fiscal agendas of the incumbent government. A development framework upheld by the state was set in motion through four consecutive post war budgets from 2010 to 2013. Its basic approach was grounded on raising the growth of the economy through infrastructure centred government expenditure while simultaneously assisting the services led growth of private investments through sharply loosening the tax framework of the economy. The monetary policy stance provided a catalyst for this process by maintaining more or less lower interest rates and stable currency through improving avenues to attract foreign savings/debt. In Sri Lankan Treasury’s terms this is expected to achieve “a real financial development of the economy” which is believed to automatically lead to a sustainable economic growth of nearly 8%. It is our view that the latter framework encouraged the growth in private sector investments which led to higher economic growth centred on services and construction activity. It however suggests that higher economic growth following the war was achieved without a fundamental shift in the economy’s growth pattern and hence, it continued the expansion of nonindustrial type investments as the dominant mode of economic growth.

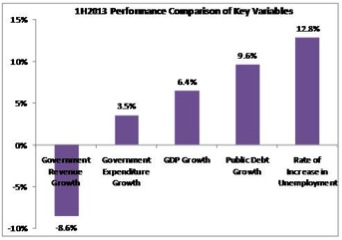

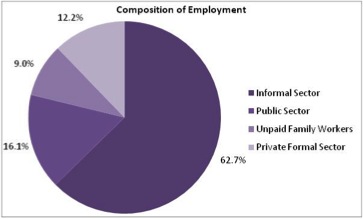

However, this particular development strategy adopted by the government although accelerated the pace of economic growth, weighed on the tax revenue position and hence the stability of the fiscal sector. The 8.6% YoY reduction in tax revenue in 1H2013 despite the economy growing as much as 6.9% YoY during the first three quarters of 2013 indicates that the broad relaxation of the tax regime in previous years although facilitated higher economic growth, it undermined the financial stability of the government. This is further indicated by the significant increase in public debt despite real growth in the economy beating regional peers. On the other hand, the higher economic growth in the face of falling government revenue further indicates that the economic growth was fundamentally based on expanding government expenditure and the growth in public investments did not in turn generate taxable incomes through increase in the formal sector employment of the economy. This is indicated by unemployment rate increasing to 4.4% in 2Q2013 from 3.9% in 2012 and 87.8% of the labour force being employed in informal sector (62.7%), public sector (16.1%) and as unpaid family workers (9%) despite economy growing at one of the highest rates in the world. Under this backdrop it is our view that the 2014 fiscal proposals are largely aimed at realigning the tax structure to improve the financial position of the government while maintaining economic growth and government expenditure without a structural transformation in the economy.

Source: Compiled according to CBSL Data

This is to say that the aim of reducing the fiscal deficit as a share of the national income in 2014 is planned to achieve through a rise in consumer and corporate tax rates while curtailing some of the tax concessions provided by previous years’ proposals. The post war fiscal agendas from 2010 to 2013 introduced numerous policy measures in the form of tax concessions and outright reductions of tax rates with a view of facilitating a higher real economic growth and raising the private sector investment as a percentage of GDP. However, in comparison, the 2014 budgets main focus is consolidating the fiscal sector while widening the prospects of higher economic growth through expansion of services sector and construction activity. This is to say the 2014 fiscal proposals retain the essential character of the development approach of the government while on the other hand distancing itself from the expansionary tax policy of previous post war budgets.

Source: CBSL and Census and Statistics Department

However, it is our belief that the continuous deterioration of the government’s revenue position and the increasing public debt levels causing the government to raise taxes and relax tax exemptions and majority of employment being created in the informal sector despite the higher economic growth rate achieved, are symptoms of a fundamental flaw in the structure of the economy, emanating from the nonindustrial pattern of growth rather than as a matter of mere financial mismanagement on the part of the government. Given that private sector appears to be having the comparative advantage in providing services and construction activity rather than in the industrial development of the economy, any attempt towards an industrial transformation will have to be initiated by the state, in line with the experience of Asia’s newly industrialised economies such as Singapore, Japan, Taiwan and South Korea.

Industrial deepening of the economy in conjunction with an industrial transformation in agriculture plays the dominant role in a development process rather than growth in services or infrastructure. The absence and presence of modern industrial expansion determines whether an economy leaps into the ranks of advanced economies or remain underdeveloped. We believe that an economic transformation will not occur if the growth process is grounded on services and construction sector expansion given that the latter are more or less a constant return to scale sector relative to industry and agriculture. Further, the main pillars of economic development which are levels of invention, technological sophistication of the production process and horizontal and vertical integration of aggregate investments and hence access to higher real wages are widely prevalent and achieved outside the development of services sector.

In this light, the 2014 budget was received with a mixed note by the public and the investment community. The increase in consumer and corporate taxes and relaxation of tax exemptions although were aimed at strengthening the fiscal consolidation process, may also moderate aggregate domestic demand on which the expansion of investments and employment are based. If the internal price levels do increase as a result of amendments to the tax structure, the domestic savings growth may tend to moderate. Hence, reliance on foreign borrowings of the economy may rise if real growth is to continue based on services and construction at 7% to 8% range. On the other hand perspective of the government rests on the belief that fiscal consolidation was undermined by the ultra lose tax policy of post war budgets which did not financially facilitate the high state expenditure based economic growth strategy.

Tax policy measures to reverse the above state of affairs include a special commodity levy on imports of many basic food items. The long list includes wheat flour, powdered milk, salt, sugar, dry fish, vegetable oils, dhal, chick peas, green gram, pasta, soups, cereals, yoghurt, butter and margarine. The budget further declared that the levy would encourage local production, but the main objective will be to raise government revenue. Before the budget, transport fares were increased 7%. Prices for building materials, including cement, aluminum and steel were also raised. The telecom levy on phone users was increased up to 25%. Excise duty on petrol was increased by LKR 2 per litre and a range of pharmaceuticals imports will be liable for Port and Air port development levy (PAL) of 5% and the NBT, export cess on spices was increased (pepper, cinnamon, clove, nutmeg and cardamoms), VAT is imposed on agricultural tractors, machinery for tea and rubber industry. The concessionary income tax of 10% applicable to firms having a turnover lower than LKR 500 million will be increased to 12% and the lower income tax rate applicable for firms with less than LKR 5 million taxable incomes was removed.

While imposing these alterations to the tax regime, the government maintained a seven-year wage freeze on public sector employees. However, the latter will receive LKR 1,200 monthly cost-of-living increase. Pensioners received an increased allowance of LKR 400 a month. The president requested private sector employers to make parallel increases. The allocations for public health was increased by a massive 24.2% YoY to LKR 117.7 billion while total expenditure on education and higher education was curtailed by 3.8% YoY to LKR 68.4 billion, possibly indicating a reallocation of resources to meet the critical health requirements of the public at the expense of funds allocated to education. The largest allocation is for the military, amounting to LKR 253 billion.

Source: 2014 Fiscal Management Report

The secondary level policy measures to support the 2014 budget’s objective include lowering fiscal deficit as a percentage of GDP to 5.2% in 2014 and 3.6% by 2016, lowering public debt as a percentage of GDP to 74% in 2014 and 70% by 2015, maintenance of the lower tax rates and achieving a LKR 109 billion revenue surplus (0.5% of 2014 GDP). Government hopes to improve the revenue surplus to 1.6% of GDP in 2015 and to 2.3% by 2016. In 2009, the IMF insisted that the fiscal deficit, which stood at almost 10% of GDP, had to be halved in return for a USD 2.6 billion loan to avert a balance of payments crisis. This further indicates that current efforts by the government to prune the deficit as a share of the GDP and convert state owned enterprises into profit making institutions are largely a result of the SBA entered between the government and the IMF in mid 2009.

The budget deficit of LKR 516.1 billion will be adding to the country’s total debt, which is around LKR 6.52 trillion, or 80% of GDP as at June 2013. Outstanding foreign debt is LKR 2.88 trillion while total domestic debt is LKR 3.64 trillion as at end of June 2013. The government is increasingly taking out foreign loans at high interest rates which will be paid through new price increases in the economy and hence inroads into living conditions. This is so given that the broad policy structure as highlighted earlier remains decoupled from achieving a fundamental transformation in the economy’s investment structure from nonindustrial to advanced industrial expansion.

On the other hand, the services which governments traditionally supply (education, health, public administration, garbage collection, transport, etc,.) do not permit the replacement of labour employed through application of machinery within the production process. Hence, they remain largely a constant return to scale sector even in the long run. For instance, the attention of a doctor, lecturer or a teacher cannot be replaced through increased mechanisation of the particular service, and the degree of mechanisation permitted within the services sector as a whole remains considerably low compared to industry and agriculture. This is to say that costs reduction through mechanisation of the production process is achieved at a considerably lower pace and in a narrow range in the services sector. Consequently, expenditure in supplying government services tends to increase over time contributing to the financial issues faced by the fiscal sector. Further, this is also the central inner dynamic shared by the Sri Lankan economy as a whole rather than the fiscal and budget deficits that are continuously highlighted. Hence, the latter phenomenon can be cited as a key reason to the prevalence of higher internal price levels and higher tendency for the supply prices to rise in the Sri Lankan economy and lower real incomes of labour compared to the regional and advanced economies. This further suggests that the relative productivity between non-industrialised service oriented economies against industrial economies may tend to widen causing the relative price level of the former group of economies to rise compared to the latter.

Government Finance

Key Highlights of Government Revenue Proceeds

Government expects total revenue and grants to rise 12.7% YoY to LKR 1,203.1 billion (13.8% of GDP) in 2013 from LKR 1,067.5 billion (14.1% of GDP) previous year. This is combined with an estimation of 22.1% YoY rise in total government revenue and grants to LKR 1,469.5 billion (14.8% of GDP) in 2014. However, 1H2013 saw total revenue falling notably by 8.6% YoY to LKR 484.1 billion. Given that government tends to receive circa 30% – 35% of total revenue during the final quarter of a year, an annualized version of government revenue could average LKR 1,059.8 billion (12.1% of GDP) for 2013. This would mean that if government revenue to reach the estimated level in 2014 it may have to rise as much as 38% YoY in contrast to the expected increase of 22.1%. Under this backdrop we are of the view that the revenue expectations of the government indicate overestimation. Further, the estimated government revenue for 2013 by the 2014 budget indicates a reduction of LKR 74.8 billion estimated from the previous year’s (2013) budget. This suggests that under falling government revenue, fiscal authorities were compelled to reduce estimates of total revenue by 0.9% of the GDP from the initial estimate in 2013.

Source: 2014 Fiscal Management Report

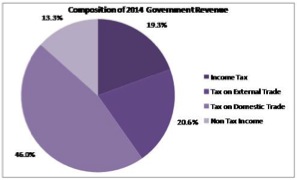

In this light, receipts from Taxes on Income & Profits are estimated to increase 18.3% YoY to LKR 283.3 billion in 2014. Government expects 22.2% of total tax revenue to be collected from the latter which is a marginal fall from 22.8% in 2013. On the other hand consumer taxes are expected to grow faster by circa 22% YoY to LKR 991.3 billion increasing its share of total tax revenue to 77.8% from 77.2% in 2013. This is to say that the emphasis of fiscal authorities on revenue collection is placed more towards consumer tax receipts, which is further indicated by the increase in consumer tax rates on a broad range of products through 2014 fiscal proposals. It however, suggests that the tax mechanism is turning increasingly less progressive. In this light government expects to increase the receipts from Taxes on International Trade (Import Duties, PAL & CESS) by 29.3% YoY to LKR 302.6 billion while receipts from Taxes on Domestic Goods and Services (VAT, Excise Duty, NBT & Telecommunications Levy) are estimated to rise 19% YoY to LKR 688.5 billion.

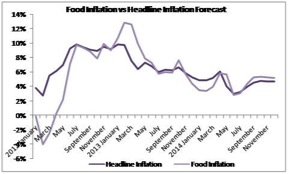

In our earlier reviews we indicated that prospects of government revenue tends to reflect an inverse relationship with the relative price of the non-taxed sector against the taxed sector, i.e., the relative price level of the agricultural food products against the price level of formal sector. This can be gauged by the comparison between the movements of food inflation against headline inflation (see Sri Lanka Country Report 2013/14 – Asia Wealth Research). Given that food prices in the economy are expected to remain relatively above headline inflation from 1Q2014 onwards, we are of the view that the relatively higher food inflation compared to headline inflation may tend to moderate the pace of government’s tax receipts during the year.

Source: ASEC Research

Hence, the possibility of government revenue remaining lower than estimates in 2014 suggests that the government may have to prune the estimated government expenditure to remain within the deficit targets as it did during the two previous years. On the other hand, more importantly, we can expect the taxes on businesses and consumers to rise further during the year 2014 given that the current tax framework may not be adequately helpful to achieve the high revenue growth expected and low deficit targets set by the government for the year. Hence, we are of the view that in order to remain within the revenue and deficit limits set by the 2014 fiscal proposals government may have to raise taxes even further during the year apart from having to prune expenditure below the level desired in the fiscal proposals. This particular phenomenon on the other hand, contradicts the conventional view which states that large scale budget deficits over the years were causing inflationary pressure in the economy. This is so given that current efforts by the government to prune the deficit is in fact raising the internal price level rather than reducing it.

Government Expenditure

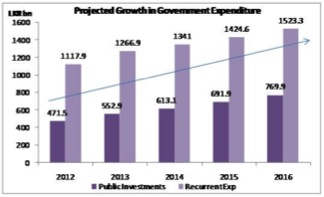

Total government expenditure is estimated to increase circa 16% YoY to LKR 1,985.6 billion (20% of GDP) in 2014E from LKR 1,712.4 billion (19.7% o GDP) previous year. On the other hand the estimated expenditure for 2013 indicated in the 2014 budget shows a reduction of LKR 73 billion from the allocation made in 2013 fiscal proposals. The reduction in expenditure by LKR 73 billion is comparable with the LKR 74.8 billion reduction in 2013 government revenue estimates by the 2014 budget. This suggests that under falling government revenue, fiscal authorities were compelled to reduce expenditure by 0.7% of the GDP in 2013 from the initial estimation.

Recurrent Expenditure

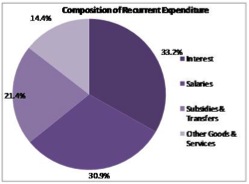

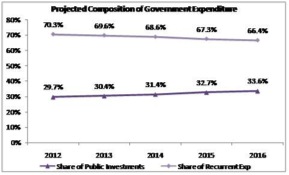

In this light total recurrent expenditure is estimated to increase 8.4% YoY to LKR 1,328.3 billion accounting for 66.9% of total expenditure, a notable reduction from previous year’s 72.3%, indicating government’s aim to shift expenditure towards public investments. Interest payments account for the largest expenditure out of all recurrent sub categories. The latter is expected to fall marginally by 0.9% to LKR 441.0 billion accounting for 22.2% of total government expenditure, a reduction from previous year’s 26%. It should be noted in this regard that the average weighted rate of interest on domestic debt has been falling while that of foreign debt has been increasing due to the change in the composition of foreign debt towards non-concessional borrowings. This may increase the outlay on foreign debt repayments of the government while cost of financing domestic debt is expected to further reduce due to the anticipated fall in domestic interest rates in 2014.

Source: 2014 Fiscal Management Report

Expenditure on salaries and wages is estimated to rise 4.9% YoY to LKR 410.6 billion in 2014E accounting for 20.7% of total expenditure, a reduction from previous year’s 22.9%. On the other hand expenditure on subsidies and transfers are expected to increase 11% YoY to LKR 284.7 billion accounting for 14.3% of total expenditure in 2014. The proposed increase in cost of living allowances of public sector employees, the increase in retirement benefits and the contributions to Provincial Councils mainly account for the increase in expenses of salaries and transfers respectively.

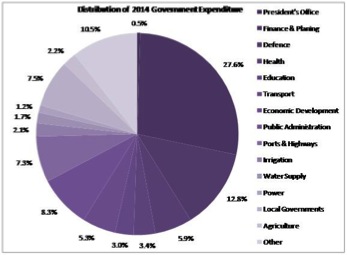

Public investments are estimated to grow as much as 32.7% YoY to LKR 668.5 billion indicating an increase from 5.8% of GDP in 2013 to 6.7% in 2014. Further, contribution of public investments to total government expenditure is estimated to rise from 29.4% to 33.7% in 2014 indicating government’s commitment to raise public investments to support and expand the spheres of growth and the rate of growth in the economy. A total of LKR 259.4 billion is allocated for capital expenditure in infrastructure development indicating an increase of 6.6% YoY. On the other hand LKR 145 billion is allocated to ports and highways development, an increase of 8.9% YoY. Higher allocations for Transport and Finance ministries have accounted for the sharp rise in the expected capital expenditure of the government in 2014. Capital expenditure of Ministry of Finance and Planning is estimated to increase by massive 271.5% YoY to LKR 63.9 billion while that of Ministry of Transport is estimated to rise 33.6% YoY to LKR 39 billion.

Source: 2014 Fiscal Management Report

Hence, private investments that have established backward and forward links with the sectors mentioned above may stand to significantly benefit through supplying government projects and through second round demand effects. Further, the demand for health, education and other essential services provided by the state sector will not be met by the government to a satisfactory level due to its deteriorating revenue position and its commitment to reduce the fiscal deficit. Hence, the inability of the state to supply the increasing demand for services that it traditionally supplies has opened up the latter for private sector investments. Given that services including education, health, garbage collection, public transport, etc which are traditionally supplied by the government do not enter international trade (i.e., they are nontradables), they remain naturally protected from foreign competition providing further advantage for the prospective private investors who are aspiring to take position in them and for those who have already done so.

Fiscal Deficit and the Sources of Financing

Fiscal deficit for 2013 is estimated to fall from 6.4% of 2012 GDP to 5.8% in 2013. However, given that government revenue did not rise as expected in 1H2013 the deficit during the period already reached 4.3% of GDP for the year. Hence, achieving the deficit target for 2013 of LKR 509.2 billion appears to be challenging given that deficit for 1H2013 has already reached LKR 378.3 billion, which is approximately 75% of the annual estimate. On the other hand, fiscal mismatch in 2014 is expected to fall to 5.2% of GDP amounting to LKR 516.1 billion. The deficit is expected to remain at this moderate level over the assumption of the fiscal authorities that government revenue may increase beyond 22% YoY in 2014.

Source: 2014 Fiscal Management Report

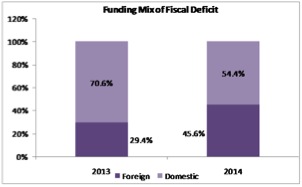

Under this back drop government expects to raise LKR 235.5 billion from foreign sources, an increase of 57.2% YoY while domestic financing is expected to fall as much as 21.9% YoY to LKR 280.6 billion. Despite the higher dependence on foreign debt to finance the deficit the total borrowings of the government is expected to marginally rise 1.7% to LKR 1,278 billion in 2014 of which LKR 1,042.5 billion are from domestic sources. On this account we expect the total outstanding public debt to reach approximately LKR 7.9 trillion accounting for 79.6% of the 2014E GDP. However, the government expects the debt to GDP ratio of the economy to reach 74% during the year. Considering the estimated lower growth in demand for borrowings by the government coupled with the prevailing low interest rate regime in world markets due to large scale and persistent quantitative easing measures adopted by monetary authorities especially in U.S. and Japan, we expect the domestic interest rates also to follow suite and dip further by 50 to 75 basis points in 2014.

How the Stock Market Interprets 2014 Budget Proposals

In terms of the secondary level policy measures noted above, the 2014 Budget contains what investors would aspire for – a lower regime of mid-single digit inflation, lower deficit, a downward interest rate regime and stable exchange rate, apart from aspiring to achieve 8% GDP growth. Further on the other hand, extension of the time period stipulated in the 2013 budget to enjoy 50% tax reduction for three years starting from 1st April 2014 for companies listing on the Colombo Stock Exchange with a minimum public holding of 20% will encourage more IPOs in the future.

Source: 2014 Fiscal Management Report

In spite of these positive developments, 2014 Budget was received with a mixed note by the Colombo Bourse mainly on the back of concern on increased tax rates coupled with a relaxation of the tax exemptions provided for businesses. Despite the not so vibrant approach of the market towards the 2014 fiscal agenda, the increase in consumer and corporate taxes and the relaxation of tax exemptions were however aimed at strengthening the fiscal consolidation process. The latter was undermined by the implementation of an expansionary tax policy which did not financially facilitate the state expenditure based economic growth strategy of the government. Hence, the aim of 2014 fiscal proposals is to bridge the gap between tax structure and the expenditure strategies which may assist sustain high economic growth rates. However, the market is likely to have responded to the immediate effect on aggregate demand in the economy by tax increases given that private investments growth is based on non-restricted growth of domestic demand.

On the other hand, more long term policy measures introduced by 2014 Budget includes reducing the fiscal deficit and public debt as a share of the GDP and continuing the relatively high growth in government expenditure on infrastructure development. However, these long term policy measures have not been viewed as providing sufficient boost to revive trading activity in the Colombo Bourse. This is to say that currently the market mechanism considers the long term trends in the economy with a lesser degree of intensity. Furthermore, it reveals that market expects the government to offer ‘fresh wave of optimism’ through each and every fiscal proposal. This was adhered to by the government during the four budgets immediately after the ending of ethnic war. However, continuation of the approach is not practical within the current context of the economy and the state of the fiscal sector and may bear on the economic stability by causing misalignment in key macroeconomic variables.

Dinuk / December 11, 2013

Sri Lanka needs a mass anti corruption movement, as in India. Today the anti-corruption party – that is a gathering of academics and activists like Yogendra Yadev has won bid in New Delhi elections..

Sri Lanka needs a third force that has the struggle against Corruption and Human Rights violations and dissapearances as its core principles..

They movement should not be led by any on the current politicians of any of the political parties since they are ALL corrupt. The politicians of the Diya wenna Parliament of Sri Lanka have amassed massive perks and are a corrupt bunch – the President and Prime Minister are the worst and must be forced to resign.

/

Dodo / December 11, 2013

And the anti-corruption movement should have the RIGHT TO INFORMATION as its first principle and lobby the corrupt parliament to pass the Right to Info. Bill – as in India.

/

Truth / December 11, 2013

The Budget 2014 is in line with the policy of reducing the budget deficit and focus on the hub strategy which excludes significant industrial growth. The Country image requires improvement. A Truth & Reconciliation Commission to deal with allegations of war crimes and improvements to law & order by revoking the 18th Amendment and the Business Takeover Act, will help to attract the foreign investments required for sustained high growth.

/