By Rajeewa Jayaweera –

Rajeewa Jayaweera

The long overdue Thirty Eighth Annual General Meeting (AGM) of the national carrier, SriLankan Airlines was held on Thursday, February 09, 2017 in the Mihilaka Medura at BMICH. It was attended by all Board members and a large number of minority shareholders comprising of former and current staff, who had received free shares at the time of privatization in 1998.

Prior to commencement of the AGM, the Chairman apologized for the long delay in publishing the Annual Report for 2015/16 and holding the AGM. He stated, “as stipulated in the 19th Amendment to the Constitution, audit work of all state enterprises including companies with a majority shareholding by the state need be audited by the Auditor General”. He further stated, “the delay was due to reasons beyond the control of the airline”.

During question time, this writer who is a shareholder raised the issue of the violation of Companies Act (17 of 2007); Section 133 (1) states, subject to the provisions of sub section (2) and of section 144, the board of a company shall call an annual general meeting of the shareholders to be held once in each calendar year a) not later than 6 months after the balance sheet date of the company (due by 30 September 2016) and b) not later than 15 months after the previous AGM (due by 15 January 2017). Further, Article 149 of the Company Articles of Association provides for the convening of the AGM within 15 months of the last AGM (due by 15 January 2017). There being no delay on the part of the company as per the Chairman, it was queried if the Auditor General had been aware of the time lines as laid down in the Companies Act as well as the Articles of Association of the company, and if the Registrar of Companies was aware of the breech of the Companies Act. The Chairman confirmed that the Registrar of Companies had been consulted.

After some time, a representative from the Auditor General’s Department who had been seated in the audience informed auditing of the airline’s accounts had been subcontracted to the audit firm KPMG due to lack of resources. She further stated, the Auditor General had required a letter from the Secretary to the Treasury (comfort letter) confirming SriLankan Airlines to be a ‘going concern’ in view of its loss-making history. This writer pointed out the requirement to circulate annual financial information 21 days prior to the AGM and queried if the Auditor General was aware, he had caused the breach of relevant clauses in the Companies Act and Articles of Association of the Company. Auditor General’s representative confirmed, audited accounts had been handed over to the airline on December 28, 2016 and there had been no delay on the part of the Auditor General’s office. At this point, the Chairman informed, the delay had been due to ‘procedural delays’.

In view of lack of ownership for the delay by SriLankan Airlines, Auditor General or any other institution, who indeed should be held responsible for the violation of the Companies Act? It must also be stated, never before in the history of the national carrier, not even during its darkest years under the stewardship of the previous Chairman has the company exceeded the time lines stipulated in the Companies Act and the Articles of Association of the company for the release of its Annual Report and holding of AGM.

In response to another question by this writer, the Chairman confirmed, the Colombo/London route was profitable on a year-round basis. He further stated, the London route was also a government requirement.

The Chairman’s Message in the Annual Report for 2015/16 states; “SriLankan recorded a strong improvement in performance during the year under review, to achieve a 26% year over year reduction in deficit. The benefit from the reduction in fuel costs was a major contributor, but our improved financial performance cannot be attributed only to fuel costs. A significant saving in procurement and fees paid to service providers and increased efficiency helped in reducing our losses.” He also states “The global operating environment in terms of lower yields and overcapacity has undoubtedly left a serious dent in our revenue, exacerbated by the currency depreciation in some of our key markets.”

However, the Chief Executive Officer in his message states; “The airline industry has seen an unprecedented year of change. The steep and largely unforeseen drop in the price of oil has led to a significant short term boost in the industry. For a short period, fares held up and the airlines were able to reap considerable profits. Since then, however, the market has reasserted itself. We have seen a similar unprecedented drop in yields (fares) in the last few months. In many cases, particularly from Europe to Asia, yields have almost halved over a two-year period.”

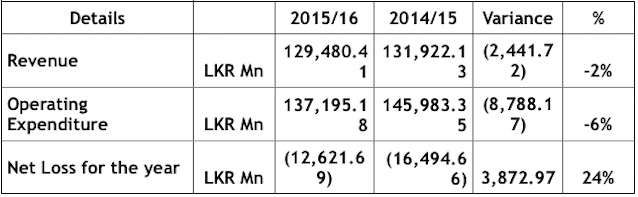

The airline recorded a LKR 12.6 billion loss in the financial year under review, a 24% reduction from previous year’s loss of LKR 16.4 billion. It included LKR 6.1 billion in interest payment and LKR 2.5 billion paid in compensation for a cancelled Airbus A350-900 aircraft. Table 1 provides a glimpse of Revenue, Operating Expenditure and Net Loss for the year under review and preceding year.

Despite the ‘short term boost in the industry’ and ‘considerable profits’ referred to by the CEO, Revenue has dropped by LKR 2.4 billion of 2% from previous year. SriLankan Airlines last recorded lower year on year revenue in 2010/11 financial year, immediately after the end of the civil war. Problem of overcapacity commenced soon afterwards with the rapid increase in capacity by foreign airlines operating to Colombo, especially the Middle Eastern carriers.

During the financial year, both Passenger and Overall Capacity have reduced by 2.4% and 2.7% respectively from previous year indicating a reduction in flights and / or distance (kms) operated. Nevertheless, number of passengers carried in 2016/17 is almost identical to the numbers carried in 2015/16.

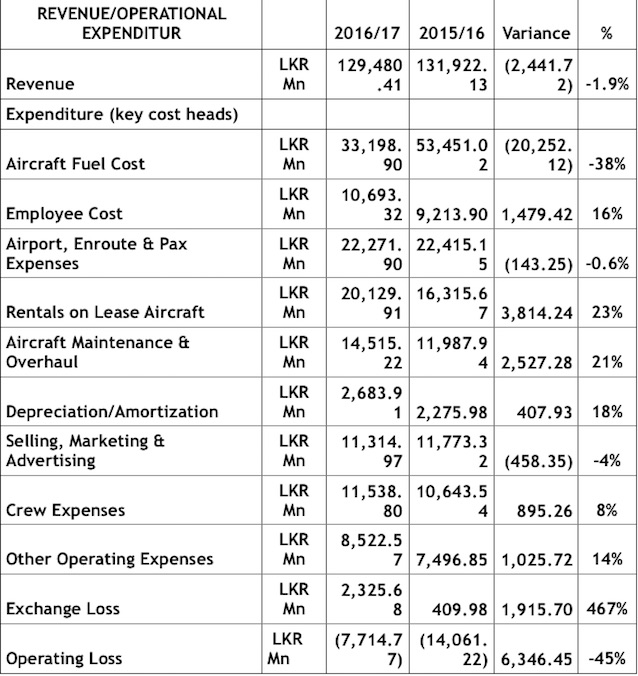

It has been stated, the ‘improved financial performance’ besides being due to the substantial reduction in fuel costs is also due to a significant saving in procurement and fees paid to service providers and increased efficiency. In the back drop of this statement, it would be pertinent to examine the operating expenditure in the Statement of Profit & Loss statement which is found in table 2.

As it can be observed, reduction in fuel cost is a massive LKR 20.2 billion, a 38% reduction from that of previous year.

Despite incurring losses, Employee Cost has increased by LKR 1.4 billion or 16%. Average number of employees in 2016/17 being 6,959, it is almost identical to that in 2015/16 of 6,987, a reduction of only 20 employees. It would appear, replacements have been recruited for staff resignations and retirements during the year, despite a LKR 2.4 billion drop in revenue and reduction in Passenger and Overall Capacity, which would generally warrant a freeze in recruitment. It would also appear, all irregular appointments made prior to January 2015 Presidential elections by the previous administration have been retained.

Aircraft rental amounting to LKR 20.1 billion, a LKR 3.8 billion or 23% increase from the previous year cannot be avoided in view of the payments falling due for the new A330-300 aircraft. Five new aircraft joined the fleet during the financial year under review.

However, LKR 14.5 billion spent on aircraft maintenance and overhaul, a LKR 2.5 billion or 21% increase from previous year is another matter and warrants an explanation. Five ageing aircraft comprising of one A330-200 and four A340-300 aircraft have been retired and replaced with 5 brand new A330-300 aircraft. New aircraft require less maintenance than those retired, most of which were older than 15 years and should have resulted in a substantial reduction in maintenance and overhaul.

Crew expenses amounting to LKR 11.5 billion, is a LKR 895 million or 8% increase from that of previous year. This expenditure mostly comprises of Crew Allowances, Hotel Charges, Transport etc. Increased expenditure does not reflect freezing of crew allowance scales and re-negotiation of hotel and transport provider contracts.

Other Operating Expenses amounting to LKR 8.5 billion has increased by LKR 1 billion or 14%. Whilst not being able to comment due to non-availability of details, it is nevertheless an indication of the lack of any cost saving.

Exchange loss of LKR 2.3 billion is an issue beyond the control of the airline.

Other than the saving in fuel cost for which the staff, Board members or the government cannot take credit, no substantial cost saving can be found in the cost heads related to operational expenditure.

In the backdrop of the lack of any significant cost saving it in operational expenditure other than in Fuel cost, the claimed ‘significant saving in procurement and fees paid to service providers and increased efficiency’ cannot be sustained.

Other Income and Gains, Finance Income, Finance Cost and Compensation for Cancellation of Aircraft Lease Agreement amounting to LKR 4.9 billion does not belong to operational expenses, nor can the Board or management be held accountable for debts accumulated prior to January 2015. When added to Operating Losses of LKR 7.7 billion, it amounts to a loss of LKR 12.6 billion for 2016/17. It must be noted, all figures quoted relates to the airline (company) and not to the group which includes the catering subsidiary.

Native Vedda / February 19, 2017

Taraki

Sri Lankan Airlines has made substantial losses in 2015/16 and 2014/15.

Is it due to Indian intervention in the domestic affairs of this island or Tamil Terrorist Diaspora’s campaign abroad?

/

Kumar / February 19, 2017

NV

Mate,you are either mad, a Modaya (idiot) or ignorant or all three. Please read Rajeewa’s article and try to understand and make sensible comment. That’s the decent thing to NV. Don’t get upset!

/

Taraki / February 20, 2017

I can assure you Kumar it is all three, but insanity dominates. The bugger is totally nuts.

/

Native Vedda / February 21, 2017

Oi Kumaruuuuuuuuuu

“Please read Rajeewa’s article and try to understand and make sensible comment.”

Rajeewa is another public racist and an anti Indian.

He has selective amnesia.

/

WarAir / February 19, 2017

Hi, I love to bitch about my obsession because I have a mole who gives me information. The mole expected to become CEO aftervenom he was temporarily made it. He sits on the board and is undermining the new CEO out of jealousy. I’m jealous because I was not selected. So every few days I have to spew my venom.

/

citizen / February 19, 2017

well,you may be right in your assumptions on the Mole within the higher echelons of the Management.This is to be expected when Board Appointments were made on political/personal considerations rather than on professional basis.Each member may have their own personal agendas to work for.

However the issue is whether what Mr.jayaweera writes(notwithstanding his source of information)has any validity .Undermining of present CEO should not be an issue if he is so competent as claimed to hold the position on one hand and if the facts are not correct as shown on the other.

If not for Mr.Jayaweera there certainly would be others as well who for their own reasons would take a dig at SriLankan affairs from time to time.It is up to the Board/Senior Management to stand up to such criticism and do what it right by the Airline and the taxpayers of this Country.

But the question is whether they are up to it ? unfortunately for the last two years or so they do not seem to have shown such capabilities

/

Jagath Fernando / February 19, 2017

If the airline cannot make money when oil is at USD 50-00 per barrel then it should be sold off or closed down.

Incompetent boards and management over many years is responsible.

Average pilot is on Rs 2 million per month with allowances and a stewardess is on Rs 500,000 per month with allowances and this cannot be sustained.

Important to note that a 500 bed hospital could be built for Rs 5 billion and the new university NSBM which could accommodate 20,000 students at a given time with state of the art facilities cost only Rs 10 billion. Sri Lankan airlines lost Rs 12 billion and Rs 16 billion over the last two years and a further Rs 15 billion loss expected in 2017!!!!

/

Rajeewa Jayaweera / February 19, 2017

To All Readers

Column 3 and 4 figures in Table 1 refers to those of 2016/17 and 2015/16 and NOT of 2015/16 and 2014/15.

The inadvertent typo error is regretted.

/

Ratnam Nadarajah / February 19, 2017

The best course of action is to sell the SOE outright, lock, stock and barrel. I know there are no takers. When Emirates managed the operation it was profitable. We all know the sorry Saga of the CEO telling the Sri Lakan government “enough is enough”, and to take the beast and do the business elsewhere.

There is no other alternative other than to ditch the beast. The power brokers should wake up at least now. One wanders, what the Havard experts told these jokers? What intrigues me most is the fact that we have gone down this route before. What is the point in trying to resurrect a dead entity. Even Moses, if he is around , would have a problem! No offence intended to Moses.

As Jagath Fernando above have rightly pointed out that we could have used the billions from the treasury ultimately from the taxpayers that’s you and me, to other worthwhile causes. May be that we are expecting too much from the Yahalpanaya outfit.

“Every adversity, every failure, every heartache carries with it the seed on equal or greater benefit”-Napoleon Hill

/

Viswajith / February 20, 2017

Mr Jayaweera has got his financial years wrong, knickers in a twist. The last published is 2015/16 and should be corrected in the article. 2016/17 financial year is still not over (Apr to Mar)

/

Rajeewa Jayaweera / February 20, 2017

To All Readers

As pointed out by Vishwajith, the financial years are incorrect.

The headline should read as ‘SriLankan Airlines 2015/16’.

This article refers to figures of 2015/16 and have been compared with figures of 2014/15. Therefore, columns 3 and 4 in Table 1 are correct whereas those columns 3 and 4 in Table 2 should read as 2015/16 and 2014/15.

Number of passengers carried and average number of employees are those of 2015/16. They have been compared with those of 2014/15.

Loss of LKR 12.6 billion is for 2015/16.

All figures have been extracted from the Annual Report of 2015/16.

The inadvertent typo errors are deeply regretted.

/

vishvajith / February 20, 2017

Who will write about UL when the setup change hands ?

As a private entity then, will we be interested ?

Delighted that my former co-worker is leaving a digital artifact of the happenings at UL. A future biz historian or biz school grad will tap into the insiders view for research process.

Btw, a phonetically sounding similar, ‘Viswajith’ contributes to the forum freely.

/

Rakitha / February 21, 2017

Thanks for all these. I wish someone else made a CEO out of someone.

/