By Kumar David –

Prof. Kumar David

Understandably the public is ultra sensitive, having survived a corrupt morally decadent regime, to any and every shortcoming of the new one. Fair enough and I encourage vigilance after a long period in which Rajapaksa putrefaction fed on the cowardice of the populace. That’s the truth. Edward Saeed remarked that the intellectual must “Speak truth to power” but he forgot to add the same injunction about speaking truth to the people. I devote this piece to two hot issues. First, what the numbers say about the Central Bank bond issue. Second, roadblocks in 19A speak truth to friends and comrades whose speechless spineless dumbness when Candidate Sirisena was twofaced about abolishing the Executive Presidency, has created to an impasse. Those who stayed silent then, that is the 99% on “our side”, are now necessarily speechless when Champika Ranawaka declares that Candidate Sirisena never promised to abolish EP.

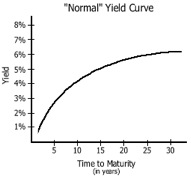

First the bond issue. Assume two examples both with 12.5% coupon (annual interest rate) but with (a) 5-year and (b) 30-year maturity terms. I have not heard of such high rates for sovereign Lankan bonds in recent debates; the highest is the Prime Minister’s mention of an 11%, 10-year, Central Bank issue. A 12.5% coupon is high for sovereign (government or Central Bank) paper; however long term bond yields need to be high to compensate borrowers for risk taking. A typical yield curve is shown. Companies go broke, revolution or war destroys governments, or as in Greece the unexpected happens. Thirty years! Good heavens, two years was too long for our Astronomer Royal; or was he on the bankroll of the Imperialists? Anyway the issuer pays 12.5% whether for 5 or 30 years and from the point of view of the public purse it’s all the same provided bonds are sold at par and one can be confident that in the long-term interest rates will not decline.

Let’s take another step and say an investor bids Rs 91 for a par 100 bond and a hard-up seller says “OK give me the 91 bucks and take it; after all I don’t need to give you the 100 for 30 more long years”. Accepting a bid at Rs 91 reduces collection though interest has to be paid on the face value. Therefore the effective interest rate goes above 12.5% – in the present case the de facto rate goes up to 13.73%. If an investor purchases a 12.5%, 30-year, bond at Rs 91, he is really collecting interest at 13.73% (12.5 divided by 0.91). What the PM’s inquiry committee needs to probe is whether a 30-year term at a real interest rate of 13.73% is unusual. To put it another way, should not the actual interest-payable on a 30-year sovereign bond be lower than 13.73%? Each one percent of ten billion is one hundred million per year for 30 years; the actuarial soundness of the decision must be challenged.

Let’s take another step and say an investor bids Rs 91 for a par 100 bond and a hard-up seller says “OK give me the 91 bucks and take it; after all I don’t need to give you the 100 for 30 more long years”. Accepting a bid at Rs 91 reduces collection though interest has to be paid on the face value. Therefore the effective interest rate goes above 12.5% – in the present case the de facto rate goes up to 13.73%. If an investor purchases a 12.5%, 30-year, bond at Rs 91, he is really collecting interest at 13.73% (12.5 divided by 0.91). What the PM’s inquiry committee needs to probe is whether a 30-year term at a real interest rate of 13.73% is unusual. To put it another way, should not the actual interest-payable on a 30-year sovereign bond be lower than 13.73%? Each one percent of ten billion is one hundred million per year for 30 years; the actuarial soundness of the decision must be challenged.

However there’s another way to look at it, that is from the point of view of the investor. What will bond (a) be worth after 5 years? Assume interest is not taken but reinvested at the same interest rate (or accumulates and compounds with the bond issuer, if allowed). In 5 years the nest-egg is worth 100 multiplied by 1.125 five times over. (Remember the compound interest formula in school?) This works out at Rs 180.2, or a profit of Rs 80.2 over five years. This averages at 16% a year not 12.5%, thanks to compounding and as compensation for taking a risk for a modest five year period.

When money is parked for longer terms a higher

return is expected as a premium for risk taking.

Here’s the catch. Take (b), the 30-year case, sit tight without touching the interest and let it compound in the same way and at the same rate. What will it be worth? In 30 years the Rs 100 is worth 100 multiplied by the 1.125 factor 30-times over. Wow, this works out at Rs 3424 or a hefty profit of Rs 3324 on Rs 100 investment! As this is over 30 years, to find the average annual rate of profit divide by 30; it is 111% per annum. The 12.5% annual interest rate seems to have skyrocketed to over 111% per year. Now include the effects of securing the 100 par bond at Rs 91; all else is the same, so a profit of Rs 3324 is made on Rs 91 investment. The average annual compounded rate of profit will be even higher; 122% (3324 divided by 30 and divided again by 0.91).

The windfall is in nominal cash-of-the-day. If inflation is a steady 5% then the earnings have to be discounted. A crude but reasonable method is to discount money at 5% for 30 years to compute its present value. If we do this, then Rs 3324 has a present value of Rs 769; divide by 30 and 0.91 as before and the return to the investor is 28% (not 122%). Still, doesn’t 28% average annual return, net of inflation, incorporate too generous a risk cushion on a sovereign bond? That question too the investigators will have to answer.

However what is far more disturbing is the following which I have been informed of with confidence by a correspondent whose name I do not have permission to reveal. Let me quote:

“Kumar

The bid prices have not been adjusted to one single cut off point in this auction. There are auctions where they do that. Here, they have eliminated bids below Rs.90.2 and accepted all bids above Rs. 90.2 up to Rs. 119 at THE ACTUAL PRICES BID BY THE DEALERS. In this process the amount purchased was increased from the pre-announced Rs. 1 Billion to Rs. 10 Billion. The lowest priced bid of 3 Billion by the Bank of Ceylon – lying at the cut-off point – is reported to be on behalf of Perpetual.

The high yield of up to 13 percent for Perpetual and the relatively high weighted yield of 12.5 percent dropped the prices of existing bonds bought previously and pushed traders into losses. You can see the pressure on the President that led to a probe within three days”.

Not only is this method of acceptance (as opposed to the usual Dutch Auction where all bidders pay at the same rate as the lowest bid accepted) grossly unfair between traders but revealing only at the auction itself that Rs 10 billion and not Rs 1 billion was to be accepted placed any bidder with inside information at an enormous advantage.

The numerical examples are didactic and illustrative; not to be taken as a case study of the current controversy. I have no opinion on the insider dealing allegation and await the report. I do wish, however, that the Prime Minister and Ministers would stop ferreting out old buddies, school mates and ideological fellow travellers and instead put men and women of sterling integrity in key positions. Lack of variety, and the absence of even one person well known to be nobody’s yes-man on this panel, dents its credibility. Of course I do not question the integrity of the three appointed members; but that’s a different matter. I have never heard of these blokes before; oh yes I can hear you mutter “That’s a big plus in their favour!”

Two big bugs in 19A

19A has been gazetted and may be pushed through with or without electoral reforms; 40 or 50 UPFA MPs will sell their mothers, sisters and country down-river than lose their pensions rights. If a 2/3 majority is unlikely, Nimal Siripals’s and Ven. Athureliya’s opposition may signal an attempt to deny a 2/3 majority, parliament should be dissolved forthwith and President and Prime Minister ask for a people’s mandate. They must declare that they will treat the results of the parliamentary election as equivalent to the outcome of a de facto referendum. They must campaign together.

Funnily, the UPFA is better off with a proportional system than first-past-the-post (FPTP) because it can smuggle a lot of garbage into the former list. Under FPTP individual candidates are well known to locals, so crooks, cronies and thugs (that is most) will be decimated. But this is not what I am griping about today. Today may be my last chance before 19A is enacted to lament that the elected-President cum elected-Parliament dichotomy is a decoction for deadlock, and secondly to moan that the so-called Council of State (CoS) is a toothless rubber stamp. I dealt with both last week (“Elected Presidency: Double-bubble toil and trouble”) but they are critical concerns and need repetition; time is running out. It will also earn me the future right to proclaim ‘I told you!’

Patali Champika Ranawaka ignores Candidate Sirisena’s Memorandum of Understanding and frequent public declarations which knowingly conveyed a commitment to the people that he would abolish EP. Was Candidate Sirisena twofaced on this issue? Yes, but is not what he promised the JHU behind closed doors but what he indubitably conveyed to the people that counts. No more about PCR; he does not matter. My grudge is with Sirisena and Ranil though both will firmly ignore it.

The immediate point is that 19A is the harbinger of a log jam. An elected president who controls parliament is a potential tyrant like Mahinda Rajapaksa; the worst excesses of that era can reappear under some dreadful future incumbent. If however the opposition controls parliament, the national leader, the President, is an immobilized dummy. Don’t be misled by the prevailing good relations between Ranil and Sirisena, the outcome of unusual antecedents, or by the fact that the incumbent president is playing a mostly ceremonial role. Constitutions must not be designed for individual circumstances; they must survive into the generic future. Not specifying the Head of Government will make current confusion and the possibility of future conflict worse. The Head of Government must be specified as the Prime Minister.

Thirty-six members of CoS are chosen by the PM and the Leader of the Opposition over a cup of tea, twenty by other parliamentary leaders – the nine ‘outsiders’ are Provincial Chief Ministers. My calculator says this assembly is 86% handpicked. Dear God must just two people nominate 36 of 65 members (55%) to the Second Chamber? Take a dooms day scenario; imagine Mahinda Rajapaksa as PM or Leader of the Opposition. He will in effect name about 18 CoS members. Since the past is our guide they will be relatives, hangers-on, flunkies and junkies.

I will not go to extremes; I concede that some people of goodwill and distinction will also be included; nevertheless they too will be preferred cynosures of two individuals who between them already dominate the other Chamber. The concept of a Second Chamber is good, so let it be filled by people’s nominees not a cacophony of flunkies. How should it be set up? Well what’s the point of wasting my breadth, who’s listening?

Bedrock Barney / March 29, 2015

Your breath is not wasted and a growing number are listening. Vasu Tissa Dew, that’s who no one listens to anymore.

/

Sengodan. M / March 29, 2015

The 19A, as it is, may not be the best one that one could have hoped for. But isn’t it something far far better than continuing with the 18A? What to do? The arithmetic of the present House compels some compromises!

Sengodan. M

/

Jagath Fernando / March 29, 2015

CBSL is in a spin at the moment due to conflicts.

1 Bond issue fiasco due to involvement of son in law and making billions within hours.

Bonds bought have now been sold and hence cannot be cancelled.

/

Plato. / March 29, 2015

The Bond issue has made Ajith Nivard Cabraal the most honourable Governor of a Central Bank this side of the Suez Canal!

/